Johan Widmark | 2025-08-25 08:00

From whole systems to modular adoption

Crunchfish’s earlier pilots in India highlighted the critical obstacle to scaling offline payments: no single actor wanted to buy into a complete, monolithic solution. The new iteration directly addresses this by separating the product into two parts: an Offline Terminal Infrastructure and Digital Cash wallets, which ensures that once the network side is enabled to receive offline payments, every PSP on that rail becomes a potential wallet customer. To accelerate adoption, Crunchfish is offering terminal capabilities for free to payment networks, betting that revenues will come from the sale of wallets to PSPs at scale. The fact that NPCI – India’s key payment infrastructure operator – has embraced this structure represents a turning point, providing Crunchfish with the launchpad it previously lacked.

Industry validation and new use cases

Beyond India, Crunchfish is widening its reach into global opportunities. The IMF recently highlighted the challenges of hardware-based offline CBDC solutions, echoing Crunchfish’s argument for wallet-led architectures. The Bank of Canada, in a retail CBDC feasibility study, recommended a two-phase commit architecture for transaction integrity – essentially identical to Crunchfish’s long-standing Reserve, Pay, and Settle model. Additional partnerships, such as with the Central Banking Standards Organization, further integrate the company’s design into emerging global frameworks. Meanwhile, Crunchfish is also rethinking cash and online payments: pilots are being prepared with a fintech serving 200,000 merchants in India for digital change in cash transactions, and new wallet features are aimed at strengthening authentication and resilience in online payments.

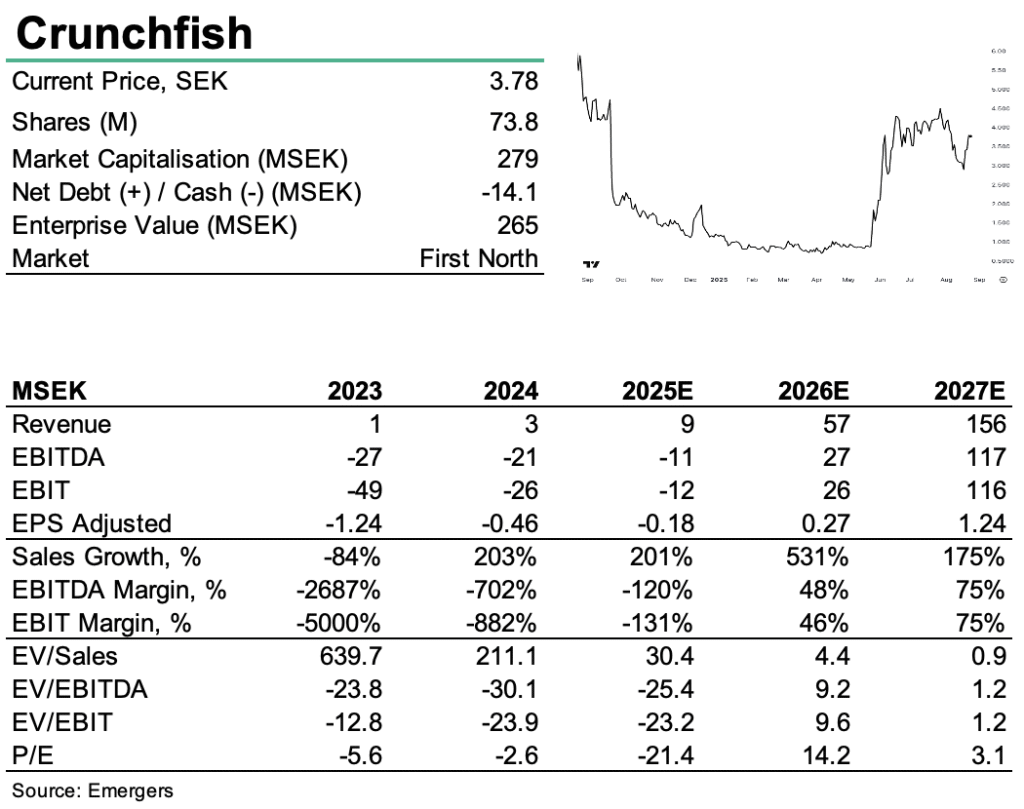

Financing needs remain: rNPV of SEK 3.2 (2.3) per share

At the end of Q2’25, Crunchfish’s cash at SEK 13.2m remain below expected OPEX for the year, and absent near-term commercial revenues the company will require additional financing to extend runway into 2027. Options beyond shareholder dilution are reportedly under discussion. Our rNPV model continues to assume 11 PSPs and 160m upfront paid users by 2028, with value capture tapering under pricing pressure, discounted at 24% with a 25% success probability. The exercise of TO11 increased the share count by 8.3m, yet the strong rally in the share price over the summer to SEK 3.80 provides a more favourable starting point for potential equity financing. Assuming a 40% discount in a future raise, the expected dilution in our model is now markedly lower than before. As a result, our rNPV estimate rises from SEK 2.3 to SEK 3.2 per share. We emphasise, however, that this remains based on assumptions with considerable uncertainty. While the equity case retains the profile of a high-risk option, industry validation from leading institutions and NPCI’s adoption of the new architecture add credibility to the possibility that Crunchfish could finally be on the path toward a viable commercial model.

See intevew with CEO Joachim Samuelsson here (in swedish)

DISCLAIMER