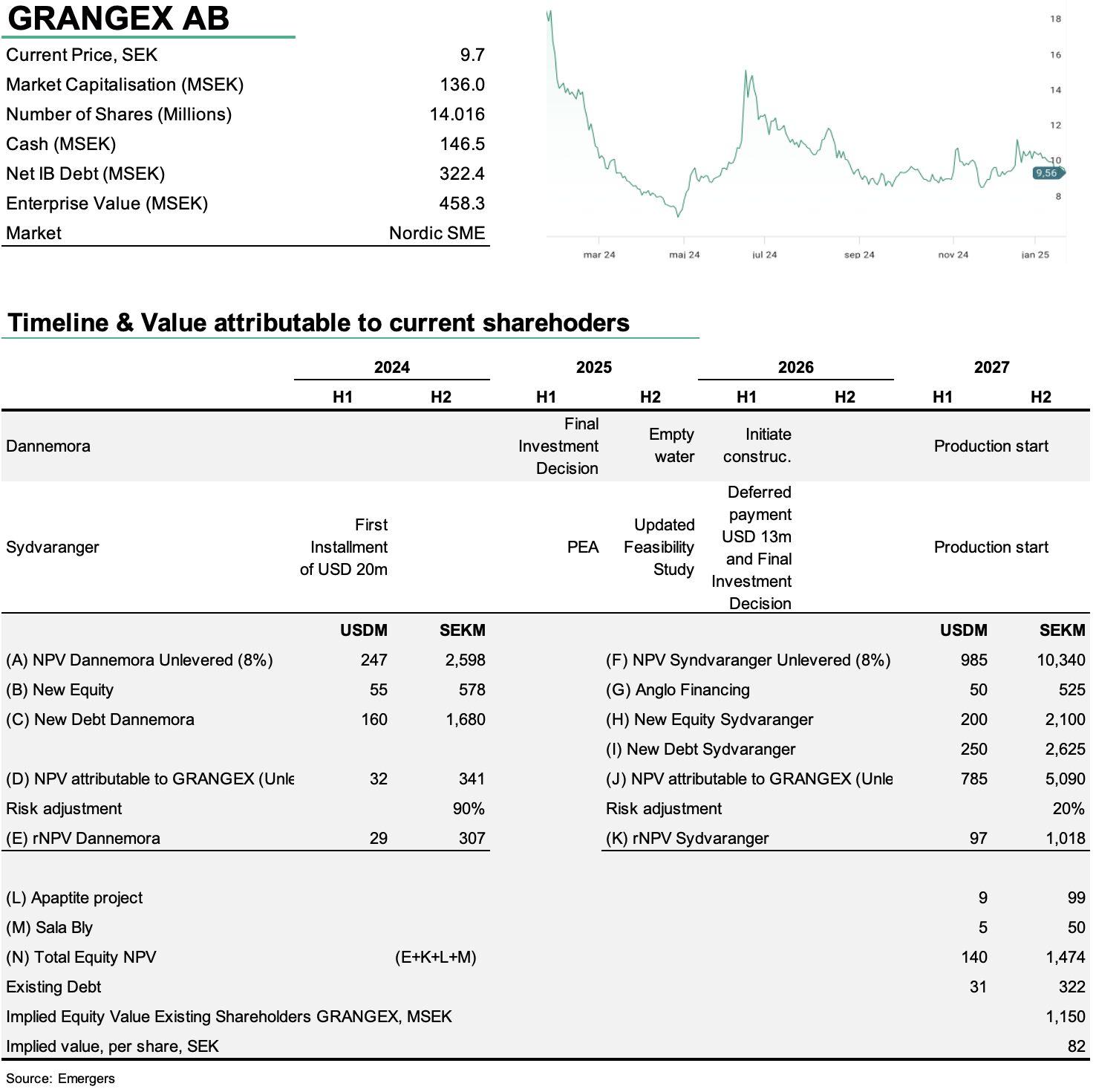

With the release of a Preliminary Economic Assessment (PEA) for the restart of the Sydvaranger mine, GRANGEX now has more clarity on the path ahead. Based on a price forecast of USD 106-145 per ton for 2027-2045, total production of 54 million tonnes of 70% ultra-high-grade iron ore concentrate, and all permits in place, the PEA supports a healthy IRR of 47% and a post-tax NPV(8) of USD 925 million. GRANGEX now targets completing a DFS for Sydvaranger by July 2025, achieving financial close in 2025, and commencing first production in early 2027. All in all, we now estimate an rNPV-based fair value for the GRANGEX share at SEK 82 per share, contingent on resolving the obstacles related to power supply at Dannemora and the management successfully raising the funding needed to develop the assets.

Johan Widmark | 2025-01-24 11:00

Option B: B for Base Case

The PEA outlines two options. The fast-track, low-CAPEX option, A, utilises the existing infrastructure with minor upgrades to enhance mill throughput. Processes will be upgraded to produce DR-grade pellet feed. Option B, which is the base case, assumes the first three years will follow Option A. Thereafter, the Bjørnevatn pit ore will be accessed at the earliest scheduled opportunity, and the crusher will be relocated to facilitate this option. This approach involves starting slower, with gradual investments, to increase capacity and access an additional 35 Mt of iron ore. The PEA presents a lower initial CAPEX than our previous estimate (USD 348m vs USD 515m) but higher total maintenance CAPEX (USD 139m vs USD 66m). OPEX, however, aligns with expectations (USD 62/ton vs USD 61/ton) and reflects a steady-state OPEX (over 15 years) of USD 54/ton. Notably, the earlier model assumed a 68% concentrate grade, while GRANGEX now targets a concentrate product with a FeMag grade above 70%.

Regarding the timeline, Option B includes a four-year construction period (incorporating Option A). Production will begin during the development phase, yielding a total 8.4 Mt of DR-grade concentrate. Steady-state production will commence in Year 5, delivering 3.0 Mtpa of DR-grade concentrate. All in all, the PEA shows a post-tax NPV(8) of USD 9 25m, slightly lower than our previous estimate of USD 1,108m.

Solid fair value support but financing remains an issue

Combined with our post-tax NPV calculation for Dannemora, we now find support for a total NPV attributable to existing shareholders, net of existing Net IB Debt of SEK 322m at the end of Q3, amounting to SEK 1,150m or SEK 82 per share. This value, however, is contingent on management successfully raising the capital needed to advance the projects. While we estimate the full financing requirement to reach USD 665m through a combination of equity and debt, Option B allows GRANGEX to start small, requiring only USD 99m in capital during Year 1. Additionally, our model shows cash flows (excluding CAPEX and financial expenses) of USD 55m in the first three years of operation, which helps ease the pressure on external financing.

Furthermore, we see a fair chance that both Anglo American (which has already committed to supporting the Sydvaranger financing package with USD 50m and could likely contribute more) and the Norwegian government, along with other public agencies, will step up to provide various forms of financial support, along with other conventional and unconventional financing institutions. Such contributions could quickly change the outlook and make the financing target appear less daunting.

DISCLAIMER