With a structural long-term growth in demand for green CO2 free iron ore and a medium-term supply crisis following the risk of a cut off from Russian high grade iron ore imports to Europe, the macro and geopolitical developments, while tragic and worrisome, are clearly beneficiary to both of GRANGX’s projects. While Q1 presented some 3-6 month delays compared to previous timeline, a weaker SEK and stronger outlook for high grade iron ore and phosphate rock prices support a upwards revision of our fair value to 0.19-0.33 (0.17-0.29) in 12-24 months, which translates to SEK 95-163 post a reversed split likely to benefit trading in the share.

Magnus Brolin & Johan Widmark | 2022-05-23 12:00

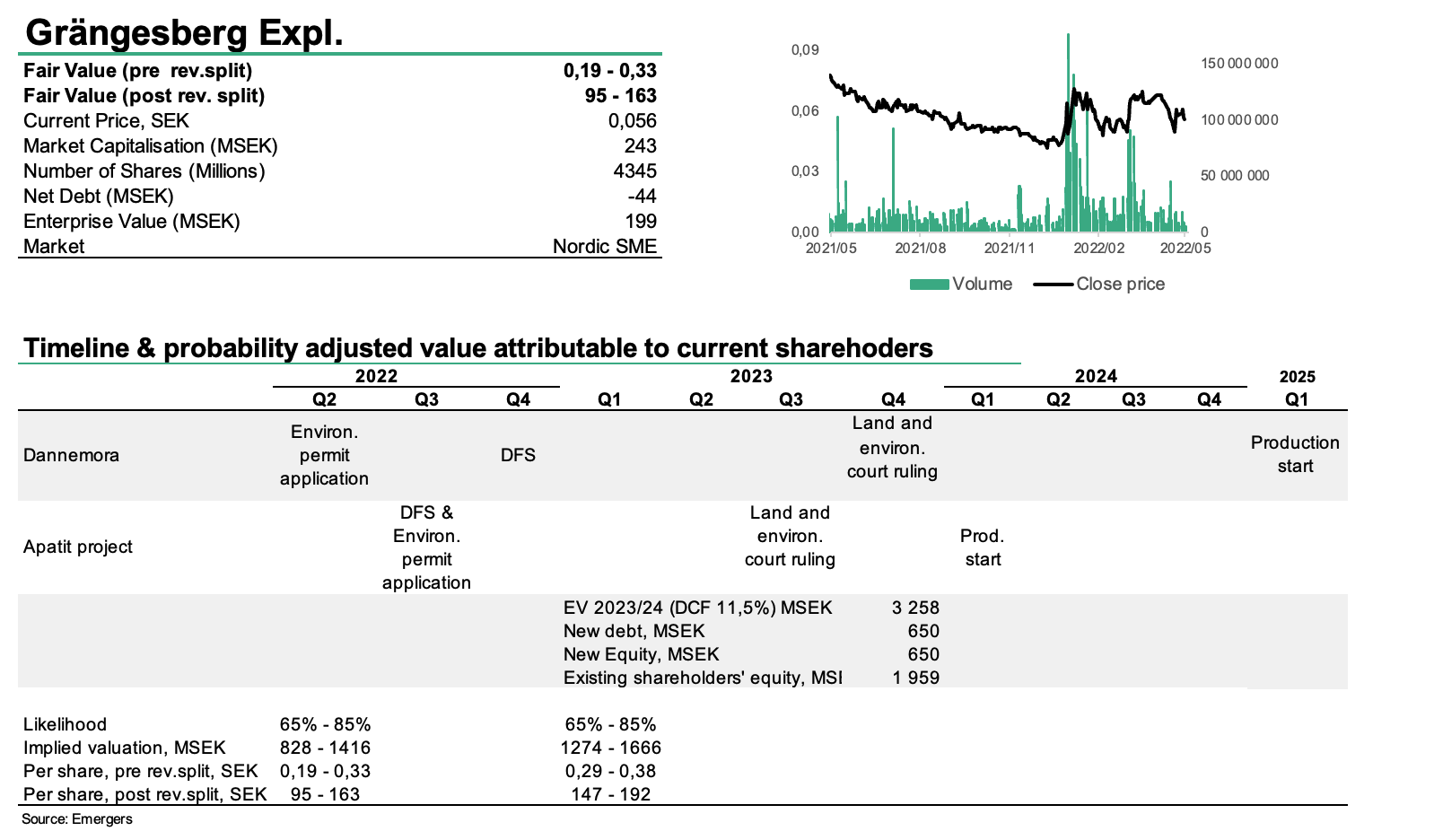

Production starts unchanged despite short term delays

Q’1 2022 saw some minor delays for GRANGX’s two projects Dannemora and Apatite of some 3-6 months each. For the restart of Dannemore to produce high grade iron ore, the submission of the environmental permit application has been delayed due to long response time from the authorities at the consultations conducted in the quarter.

The Apatite project on the other hand was delayed due to technical issues at an external laboratory. With these issues resolved, the company expects to submit the environmental permit application for Dannemora later in Q2, and for the Apatite project this summer (Q3) and present the DFS for Dannemora in October. With the major financing round for these projects most likely during H1’23, we maintain our projection of production start in the Apatite project around winter ‘23/24 and production start in Dannemora around winter ‘24/25.

Significant tailwind from sanctions on Russia

As a consequence of Russia’s invasion of Ukraine and the subsequent sanctions, the European steel and iron ore industry is now under increasing pressure as more than 20% of European imports of high grade iron ore and pellets risks being cut off. This lends further support to our expectation of a continued expansion of the price premium for higher grades, such as the best in class 68% quality to be produced at Dannemora.

This emerging supply crisis can also be noticed in Sweden where resource security of supply and self-sufficiency rapidly has risen on the political agenda. Combined with the planned CO2 free production profile at Dannemora, this is likely to provide some soft support to GRANGX’s forthcoming environmental permit application.

Likewise, the war in Ukraine and subsequent trade restrictions have also affected supply of phosphate rock, which is an integral part of the vital fertilizer industry, where prices have surged from 100-150 to 250-300 USD/t. To be prudent, we only incorporate a very small part of these price changes into our valuation model, but note that it provides a very bright backdrop for the projects which will enhance both GRANGX’s chances to finance the projects at attractive levels in H1’23 as well as the chances to include some form of trade financing into the mix, should management wish to do so.

Mix of prices, FX and risk premium net positive to fair value

The aforementioned price developments and a 10% depreciation of the SEK year to date, support an upwards revision of our DCF-based fair value for the share. On the other hand, the turmoil on financial markets, with waning stock prices and rising risk premiums also affect GRANGX’s financing cost, both cost of equity and cost of debt, meaning that we’ve raised our WACC to 11,5%. All in all, this supports a very healthy financial profile, with a NPV at SEK 3.2bn and a repayment within three years. Reduced by project financing for both the Apatite project and Dannemora, where we expect debt of SEK 650m and new equity of SEK 650m, approximately SEK 1,959m remains attributable to today’s shareholders. With an estimated probability of successfully passing the next two years’ milestones of 65-85% per year, it provides support for a fair value today of around SEK 828-1,416m or SEK 0.19-0.33 per share (0.17-0.29). After the decided reversed split of 1:500 this translates to 95-163 per share.

Should the management decide to include a trade finance solution into the financing mix, this would probably cap some of the upside with regards to rising iron ore and/or phosphate rock prices, but also limit shareholder dilution and raise potential further.

DISCLAIMER