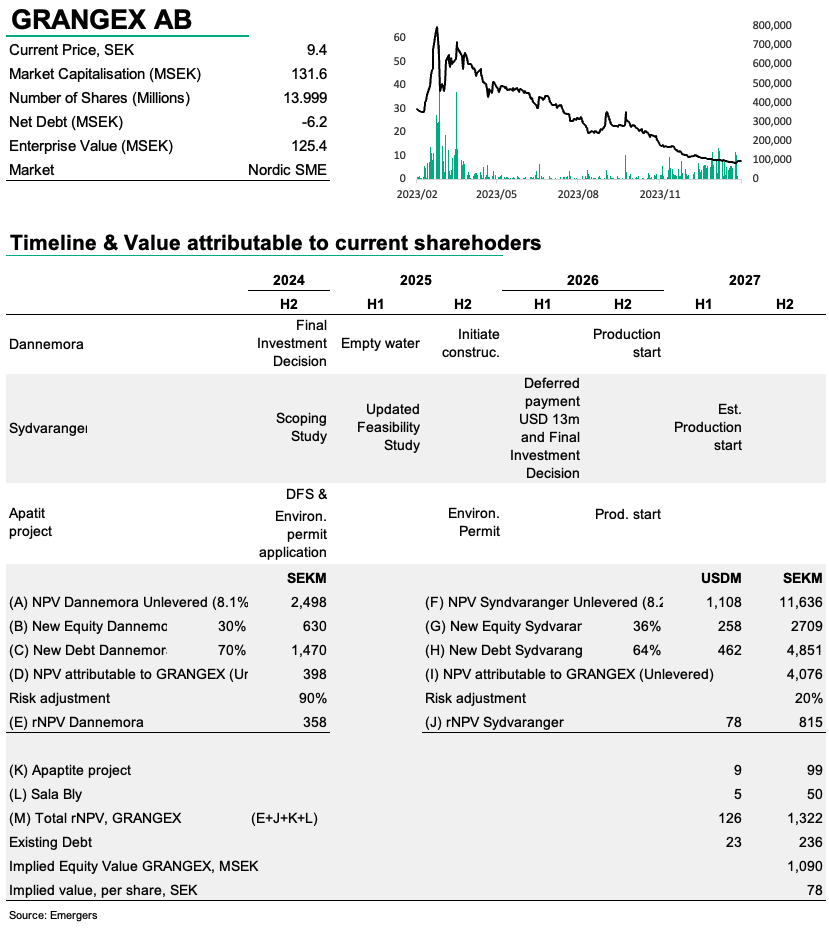

With a striking renegotiation of the final purchase agreement for Sydvaranger, reducing the initial payment from USD 1+19m to USD 1+0.5m, GRANGEX succeeds in avoiding both diluting existing shareholders and bringing in equity partners in Grangex Sydvaranger AS, as was the previous plan. Combined with issue proceeds and the finalized USD 17.5m offtake agreement with Anglo American, GRANGEX is now set for the next step where a Scoping Study and Feasibility Study will determine a new mining plan and a new tailings disposal method. With an updated feasibility study for Dannemora expected before summer, and final project financing and investment decision soon thereafter, and new plan for Sydvaranger, we see several triggers in the coming 12-24 months that should drive a revaluation of the depressed share. Our NPVs include a high degree of uncertainty especially for Sydvaranger, but we still find support for a total rNPV-based fair value for today’s equity holders upwards SEK 78 (55) per share.

Johan Widmark | 2024-05-08 10:00

Favourable renegotiation of final terms for Sydvaranger

From initially expecting to pay USD 20m (USD 1m in 2023 and USD 19m in Q1’24), GRANGEX in the end managed to renegotiate the payment to USD 1.5m of which USD 1 was already paid and a mere USD 0.5m is now paid on closing. The deferred consideration of USD 13m to be paid on final investment decision (expected in 2026) remains unchanged. GRANGEX also assumes USD 25.5m in debt that matures on Dec 31st, 2025.

Soon thereafter, GRANGEX also announced the closing of the offtake agreement with Anglo American Plc. in which Anglo will purchase all life-of-mine ultra-high-grade magnetite concentrate production from the Sydvaranger Mine. Anglo has paid USD 17.5m for a royalty of 3% of revenue, while also committing to contribute USD 50m to finance the restart of Sydvaranger at final investment decision. Grangex Sydvaranger will immediately use USD 3m of the royalty proceeds to reduce the assumed debt to USD 22.5m, while the remaining USD 14.5m will be used to complete a new feasibility study and the current care and maintenance program at the Sydvaranger Mine, running at an annual cost of USD 5m.

The first step in GRANGEX’s plan for Sydvaranger is to make a new optimal mining plan, confirm a direct reduction grade product specification as well as new tailings disposal method. Based on an existing feasibility study from 2020, the Sydvaranger Mine has the potential to produce up to 4 million tonnes per year of ultra-high-grade concentrate for a period of 25 years. But should GRANGEX utilize the current permitted sub-sea tailings disposal method this would cause Anglo to buyback the royalty agreement.

Set for now, but major raise on the near term horizon

With an estimated SEK 61m net in proceeds from the rights issue in Q1, cash at SEK 34.5m at Dec 31st, 2023, the USD 0.5m payment for Sydvaranger, USD 17.5m royalty payment from Anglo American of which USD 3m has gone to reduce debt, we now estimate cash before operational costs to date at around SEK 240m. GRANGEX has already assumed responsibility for the USD 5m in care and maintenance costs at Sydvaranger since Jan 1st, 2024, and the remainder of proceeds are expected to fund the continued development of Dannemora and Sydvaranger.

In Dannemora, an updated feasibility study was initiated in December, which will define the total CAPEX, and thus the total financing requirement. Project financing and investment decision were previously planned to be completed during Q2’2024, but we now expect that to be somewhat delayed into H2’24. The start of the mine drainage is planned to begin as soon as the investment decision and full project financing are in place. As a consequence we now postpone our expected production start to H2’2026.

Along with the case in Dannemora that already offers good potential value for shareholders, we have now included Sydvaranger into our rNPV calculation, although we highlight that uncertainty in this side of the model is markedly higher, at least until the company presents an updated Feasibility study. That being said, the first data points from Sydvaranger indicate an even greater potential than in the previous DFS (i.e. an NPV well above USD 550m) when raising the output from blast furnace concentrate to direct reduction iron ore, and accounting for significantly higher iron ore prices.

Key milestones for investors

After the short-term financing round now completed, we look forward to:

• updated DFS and commencement of drainage of Dannemora in H1’24

• updated DFS for Sydvaranger later in 2024

• the major capital raise slated for 2024

• Production start in Dannemora in 2026

• Final Investment Decision for Sydvaranger in H1’26

DISCLAIMER