Andreas Eriksson | 2021-10-20 10:05

Transformation into an industrial company with an undivided focus on High Performance filters

With the acquisition of the last remaining 15% of the shares in Eagle Filters, Loudspring is now increasing its ownership to 100%. The seller is Eagles founder Juha Kariluoto. In connection with the acquisition, Loudspring also restates its strategy of transforming Loudspring into an industrial growth company with an undivided focus on Eagle Filters’s business. The step is motivated by the fact that Eagle has been identified as the holding with the greatest value-creating potential, both for shareholders and for the climate. The price for the shares will be based on Eagle’s future EBIT during 2022 – 2024, and payments will be made in increments between 2023 – 2025. From a stock market perspective, the acquisition will mean a completely new level of transparency in Eagle, as the company has so far not had its own reporting available to Swedish investors. Industrial companies also enjoy higher valuation multiples than investment/holding companies.

High-performance filter solution for gas turbines

Eagle manufactures high-performance air filtration solutions for gas turbines that contribute to more efficient fuel utilization, higher energy production and extended turbine life. The market today is dominated by filters of lower quality where the rotor blades are broken down by dirt, which leads to poorer performance and thus poorer production. Eagle so far has only a small market share of the approximately 10,000 gas turbines around the world that can use the filters that Eagle manufactures. But looking only at the company’s existing customer base, a complete conversion to Eagle’s products, in all of these existing customers’ gas turbines, would translate to more than 10-fold growth for Eagle.

– We provide energy efficiency technology where it matters most – for the world’s largest point emitters of CO2. Eagle’s technology is being used by some of the world’s largest energy utilities and has potential to grow for the foreseeable future. Eagle Filters also has extensive competence in filter materials, and we will focus all our resources to help Eagle Filters maximize its potential, says Jarkko Joki-Tokola, CEO of Loudspring.

Filter for both today’s and tomorrow’s gas turbines

According to market research company Mordor Intelligence, natural gas accounts for more than 23% of the world’s energy production today. As a power source, gas emits 50% less greenhouse gases than oil, but with a significantly larger footprint than solar and wind power. The importance of solar and wind power will certainly only become even greater, and here Eagles’ filters can play a crucial role in balancing the supply of energy in renewable production. As is well known, solar cells do not generate energy when the sun is not shining, but the excess from the solar hours can be converted into hydrogen, which can then be burned in gas turbines by the kind the Eagles’ filter makes more efficient. This hydrogen combustion holds a potential for Eagle that is easy to overlook at first glance but offers a high future potential.

Surging prices for emission rights benefit demand for Eagle

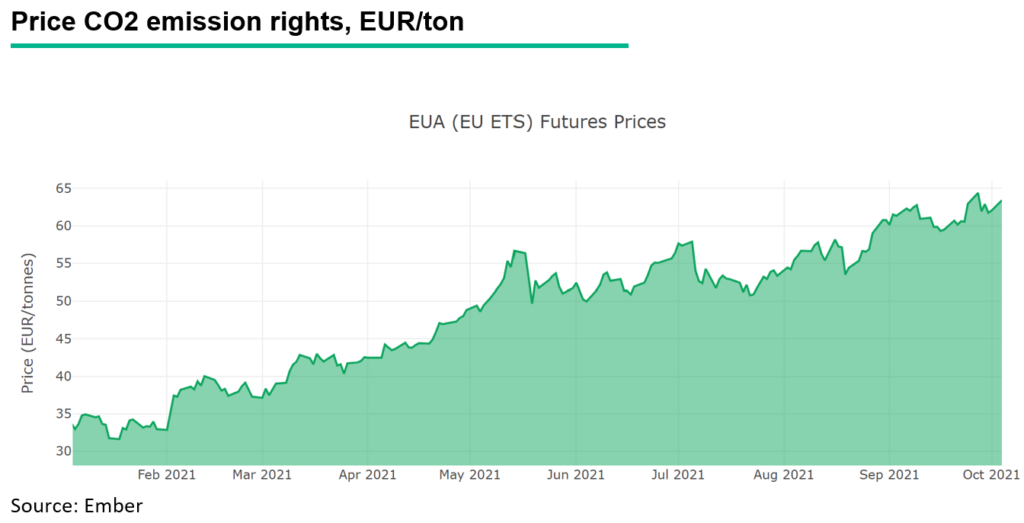

In 2020, Eagle Filters reduced its customers’ carbon dioxide emissions by around 150,000 tonnes, a figure that is particularly interesting in light of the fact that the price of emission rights in the EU has increased by almost 100% since February this year, which provides further support for demand for Eagle’s filters. After two years of flat growth as a result of the pandemic, Eagle is now heading towards impressive growth in 2021 and with a record size pipeline for 2022. Loudspring already has a revenue target for Eagle of 3.3 – 4.5 MEUR for 2021 and 4.5 – 6.0 MEUR for 2022, which does not include Eagle’s new business area, respirators. With the concentrated pipeline and eased pandemic restrictions, we see good chances of a substantial growth boost in 2022, up to Loudspring’s anticipated levels. An assumption of an EBITDA margin of 20%, in line with the listed peers Donaldson Company and 3M, would mean an EBITDA well above 2 MEUR 2022. As for the remaining holdings, Loudspring has not yet announced their intentions, so it remains to be seen what will happen to Loudspring’s 38% stake in Nuuka Solutions, 20.5% in Sofi Filtration and 13.2% in Enersize, among others.

Read more about Loudspring’s Eagle Filters here

DISCLAIMER