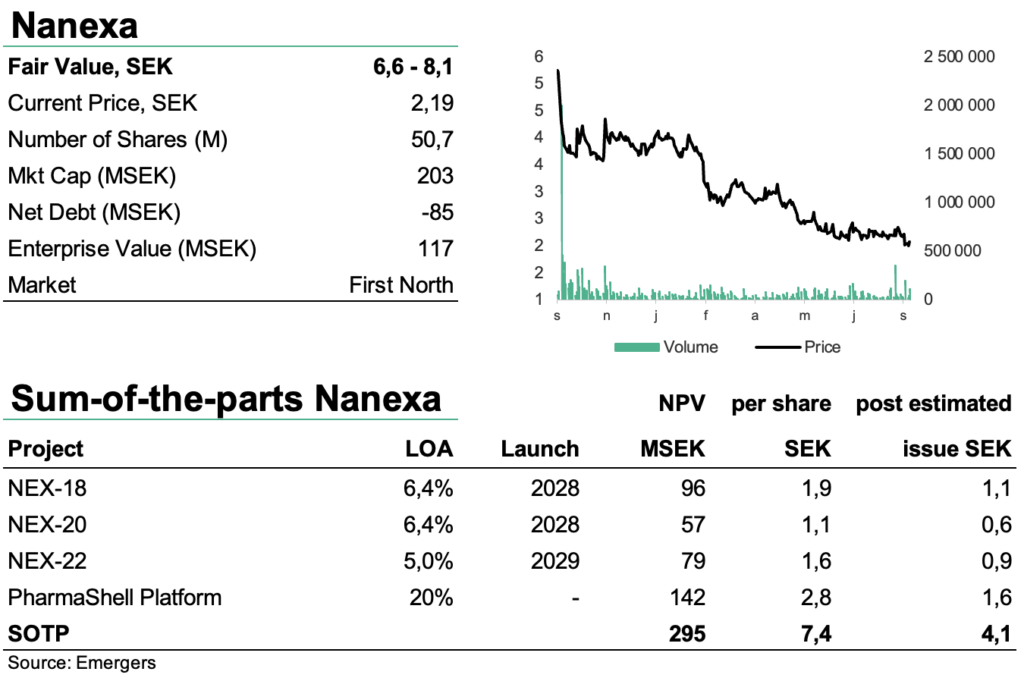

Nanexa’s next proprietary development project, NEX-22, is a long-acting formulation of liraglutide for treatment of type 2 diabetes (T2D). Addressing a growth vertical within the USD 50bn type 2 diabetes market, the project is expected to enter phase I in 2023 and with a blended 5,4% likelihood of approval, NEX-22 alone could add some SEK 2 to per share to our rNPV. Simultaneously, investors return requirements are rising and with another capital raise likely on the horizon, we now find support for a fair value of SEK 6.6-8.1 per share (6.3-7.7), which a potential issue at SEK 2 per share could cut to SEK 4.1, still providing a significant upside with plenty of milestones ahead. Should we however see a first firm license development agreement before that, this could alleviate the need to raise more cash.

Johan Widmark | 2022-09-16 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Significant benefit for patients suffering from diabetes

Nanexa has now announced its third proprietary development project, NEX-22, a long-acting formulation of liraglutide for treatment of T2D. With 50 million people diagnosed with T2D in the seven major medical markets it is one of the most common lifestyle diseases and expected to continue to grow. Liraglutide is a so-called GLP-1 (Glucagon-like Peptide-1) analogue. Today, diabetes treatments are a USD 50 bn market, where GLP-1 analogues account for about USD 15 billion, of which Novo Nordisk, makes up over half, and is expected to grow market share fast in the coming years. However, their main liraglutide drug Victoza will go off patent in 2023.

Today patients on liraglutide take a daily injection of the drug, which Nanexa hopes to replace with a monthly long-acting injectable. One study shows that only 50% of patients suffering from T2D is taking their prescribed injections, which means that improving patient adherence could have significant positive effects on treatment efficacy and cost for the healthcare system.

Targeting clinical trials for NEX-22 in 2023

Nanexa already have a plan for pre-clinical and clinical development of NEX-22, with the expectation to start clinical trials already in 2023. With Novo Nordisk’s Victoza (liraglutide) going off patent in 2023, it’s generally expected to see market share drop from 30% in 2019 to 2-3% by 2025. Together with Novo’s other liraglutide drug Saxenda, Victoza account for over a quarter of Novo Nordisk’s GLP-1 revenues, which is why we calculate for a potential peak market share of 5% for NEX-22.

Based on a 10% royalty rate and a 15% discount rate risk adjusted with a blended statistical accumulated likelihood of approval for off-patent, chronic rare and autoimmune diseases of 5,0%, we arrive at a rNPV of around SEK 80m or SEK 1.6 per share.

Eventful year ahead

With the initiation of phase I with NEX-20 (a long acting injectable of lenalidomide for the treatment of multiple myeloma) in Q4’22 and the restart of clinical trials of NEX-18 in 2023, we expect an eventful period ahead. While the new facility will increase costs going forward, we believe it will have a positive effect on the chances for a platform licensing deal for PharmaShell, which would lessen the need for additional financing while also providing an important reference point for the value of the platform, and most likely work as a positive trigger for the share. At present, Nanexa is financed for continued development into H1 2023.

As all early development companies, Nanexa continues to be affected by the general low risk appetite that is rewarding near term cash flows and punishing profits far into the future, pushing up investors’ return requirements. After a hike in model discount rate to 15% we find that a risk-adjusted NPV for NEX-18, NEX-20, NEX-22 and the platform PharmaShell (1.9 + 1.1 + 1.6 + 2.8 SEK per share) provides support for a fair value of SEK 6.6-8.1 (6.3-7.7) per share.

DISCLAIMER