Johan Widmark | 2023-05-05 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Phase I results for NEX-20 before end Q2

As announced in Q1, Nanexa had a positive outcome in the first preclinical study, a one-month study in rats, with NEX-22 for treatment of type 2 diabetes. The results show a controlled release of liraglutide for 28 days, compared to 2 days for a formulation with liraglutide (Victoza) without the PharmaShell coating.

Besides the success for NEX-22, the results also have implications for Nanexa’s collaboration with Novo Nordisk, as well as other potential peptide drug substances for which the PharmaShell platform can be used to produce long-acting formulations. In addition, phase I with NEX-20 (a PharmaShell-coated a one-month depot preparation of lenalidomide for treatment of multiple myeloma) is proceeding according to plan and is expected to be completed before end of Q2’23.

Revising our model and adjusting for another raise on the horizon

Revenue in Q1’23 amounted to SEK 8.2m, where SEK 2m was from evaluation agreements for PharmaShell. SEK 5.6 was a periodization of the prepaid USD 4m fee from Novo Nordisk. With OPEX at SEK 18.8m, cash flow amounted to SEK -20.7m in Q1, meaning that the cash position of SEK 60.5m gives the Company some three quarters of runway, but not more.

This highlights the need to secure additional funding during the summer semester. Since license and further exclusivity agreements seem premature, it will most likely be in the form of a rights issue. But with a strategic industry giant such as Novo Nordisk as Nanexa’s largest shareholder, chances to secure continued financing should be good.

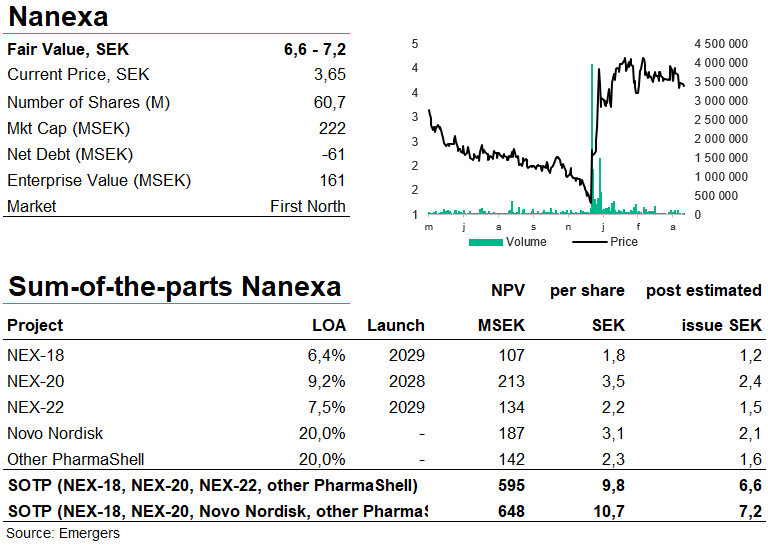

After the progress in pre-clinical trials with NEX-22 and the forthcoming completion of phase I with NEX-20, we’ve updated our valuation model and probabilities. Combined with a rights issue of some 30m shares to raise another year of runway (SEK 80m) at an estimated 25% discount, we now find support for a fair value of SEK 6.6-7.2 (6.6-8.2) per share. After the results of phase I with NEX-20 at the end of Q2, we now look forward to initiation of Phase I with NEX-22 later in 2023 and NEX-18 (long-acting injectable azacitidine for myelodysplastic syndrome) most likely in 2024.

DISCLAIMER