Johan Widmark | 2023-09-22 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

SEK 107m injection secure broad set of activities in 2024

Of the net proceeds of SEK 107m after costs, around 30% will go to NEX-22, for treatment of type 2 diabetes, for the implementation of phase I, preparation and initiation of phase II and advisory meetings with FDA regarding continued clinical program. 15 % will go to NEX-20 for completion of the Phase Ia clinical study, and preparation and initiation of dose escalation study, Phase Ib, in patients with Multiple Myeloma. 20% will got to further development of PharmaShell to broaden the use in biological medicines, e.g. peptides and monoclonal antibodies while 10% will be allocated to business development aimed at broader development/licensing agreements. 10% will go to preclinical evaluation of NEX-18 and the rest to production and general admin.

Subscription price is set at SEK 1 per share which is a pretty steep discount compared to previous close. At 121,4m new shares this will mean a 67% dilution for non-participating shareholders.

Wide range of outcomes

Earlier in H2’23, Nanexa announced the initial positive PK data for NEX-20, showing a controlled release of lenalidomide. Now, Nanexa expects the full PK profile, safety and tolerability data later in H2’23. Primary focus however seems to be on NEX-22 where Nanexa expects to submit the clinical trial application later in H2’23 with initiation of phase I in early 2024. NEX-22 is a long-acting depot formulation of GLP-1 agonist liraglutide. Liraglutide is currently available as a once-daily injection, but NEX-22 is designed to be injected once a month, meaning a significant improvement in convenience for patients, and adherence.

This runs in parallel with Nanexa’s evaluation agreement with Novo Nordisk for an unspecified target. Our base-case assumption is that this is most likely to be other GLP-1 Semaglutide, now accounting for over 1/3 of Novo Nordisk’s revenues, with very positive growth prospects. In Q2’23, 45% of Novo Nordisk’s revenues were for some GLP-1 drug. We now see a 30% probability for a license deal with Novo Nordisk, estimating a 3% royalty fee in such a deal. A rough assumption the application of PharmaShell on 10%-40% of Novo Nordisk’s portfolio corresponds to a SEK 250m -1bn NPV for the Novo Nordisk deal alone. But all estimates with regards to Novo’s potential application of PharmaShell, pricing strategy and customer segmentation are highly uncertain.

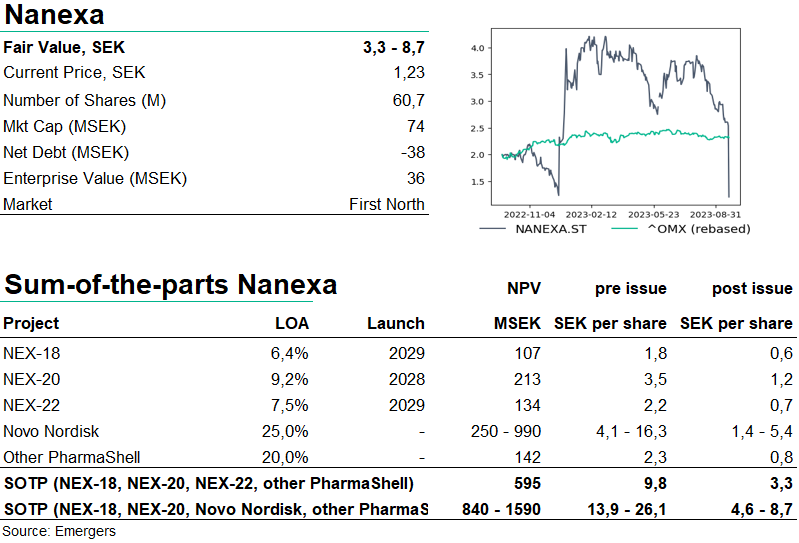

Translating to a wide valuation range

The wide range of outcomes, especially with regards to potential applicability of PharmaShell on Novo Nordisk’s products in the event of a license deal, means that it’s near futile to try to pin down a single number in a valuation of Nanexa. It is however worth noting that the standalone pursuit of NEX-22 is most likely mutually exclusive with a license deal with Novo Nordisk. In our Sum of the Parts valuation, this gives support for a valuation range anywhere between SEK 600m and 1.6bn, corresponding to SEK 3.3-8.7 per share post issue. This compares to our earlier fair value at SEK 6.4-7.7 per share which however was based on the expectation of a SEK 80m share issue at 25% discount.

So, after the right issue set to be completed in October and the results of phase I with NEX-20 later in H2’23, we look forward to initiation of Phase I with NEX-22 and NEX-18 (long-acting injectable azacitidine for myelodysplastic syndrome) in 2024.

DISCLAIMER