Johan Widmark | 2022-03-01 08:00

Orders year to date amounting to half of sales in 2021

The two fucoxanthin orders in Q1’22 with a total value of 3 MSEK, corresponds to roughly half of the company’s total sales in 2021 at 6.1 MSEK, of which 4.5 MSEK also was fucoxanthin. This clearly illustrates not only that this has now become Simris’ by far most lucrative business, it also shows that the B2B-segment is the right strategic path for Simris and that the company is now on track to capitalise on the growing demand from the nutritional, cosmeceutical and pharma industries.

As for the omega-3 vertical, Simris has decided to withdraw its EFSA Novel Food application, partly because Simris will most likely use a higher yielding stem for its omega-3 product, but also because of Simris’ change in business focus to the considerably more valuable fucoxantin.

International micro algae space gaining momentum

In a global perspective, the micro algae industry has attracted considerable VC financing in the past five years, which along with the M&A-activity ranges into several hundreds of million USD. At the same time, the whole microalgae market can still be considered to be in its infancy, as various market research firms estimate the total global market (excluding biofuels) to be less than 1 BN USD. By 2028, market research firm Meticulous Research, expect the global microalgae market to amount to 1,8 BN USD, representing a 10.8% CAGR in 2021-2028.

In terms of peers, Paris listed Fermentalg is valued at 105 MEUR, supported by sales of 5.6 MEUR. While that is next level compared to Simris, the 18.8x sales multiple clearly illustrate the premium multiples international investors are willing to pay for exposure to the emerging micro algae industry.

Time to capitalise on unique micro algae platform

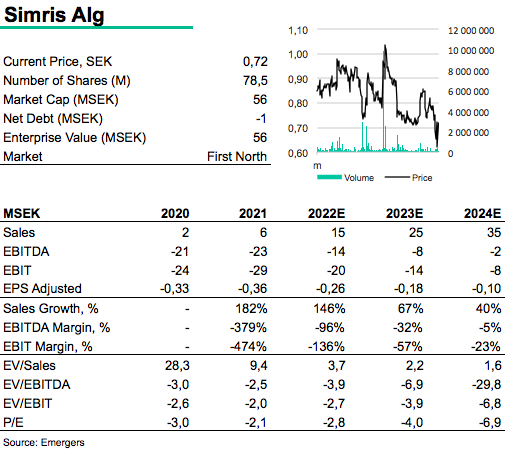

We have long argued that Simris has a unique micro algae platform that offers considerable opportunities in an international perspective and that the announcement of new B2B deals is the key to unlocking this potential. Unfortunately, the share still suffers from a crisis of confidence stemming from previous management and an historic overemphasis on the short-term sales development of the omega-3 product line. With sales in 2021 at 6.1 MSEK, Simris managed to surpass our previous sales expectation at 4 MSEK. With the orders to date we have updated our revenue expectations for 2022 from 12 MSEK to 15 MSEK, which also includes our lowered expectations for the omega-3. Chairman Steven Schapera has also communicated considerable cost cutting measures, but we expect that a scale-up is associated with increased sales, marketing and R&D spend, meaning that we still do not expect Simris to show profit in 2022-2024.

While the two fucoxanthin orders to date will be delivered from existing inventory, the liquidity situation can be described as tight, with cash at 31 Dec 2021 below 1 MSEK, and we expect some sort of capital raise in the near future. This will probably be communicated in conjunction with the appointment of a new CEO, which remains one of last key pieces of the puzzle.

So all in all, we continue to see a significant revaluation potential in Simris, and that the triggers are now starting to line up. We apply a 6x sales multiple to our forecast for 2023 (derived from a third of the sales multipe of Fermentalg) to arrive at a 150 MSEK or 1,9 SEK per share fair value in 2023, but stress that this is before adjusting for any dillution in an expected capital raise.

DISCLAIMER