Johan Widmark | 2022-09-07 11:30

Acquisition to accelerate entry into Biopharma

Cyano Biotech GmbH. hold what is probably one of the world’s largest libraries of cyanobacteria, comprising more than 1,100 producer strains. Having identified more than 5,000 novel, natural, compounds, the acquisition is right in line with Simris’ long-term objective to accelerate revenue generation by selling high-value, high-margin biological products to the Biopharma, Cosmetics and Nutrition industries.

In addition to accelerating Simris’ entry into pharma and providing Simris with its own internal R&D capability, the acquisition is expected to deliver a number of synergies for cost efficiency. Cyano Biotech have had an average turnover of over EUR 0.5m over the past two years and is expected to deliver an EBITDA in the region of EUR 100k in 2022.

Two-fold deal

Overall, there are two parts to the deal:

1. Payment for the ADC platform: Total max value of EUR 10.24m

• EUR 1.0m in cash + EUR 120k in shares paid on the day of closing

• EUR 1.0m in cash + EUR 120k in shares paid 12 months after the day of closing

• Earn-outs paid at a rate of 10% on net revenue from sales of the ADC platform, up to a maximum of total value of EUR 8m more

2. Payment for revenue from the non-ADC business:

• 10% of revenue from sales, through to 2025, converted quarterly into Simris shares and a quarterly basis

In relation to the earn-outs, these will only be triggered by revenue generated from the ADC platform. For example, if Simris secures a contract with a Pharma company and they pay EUR 1.0m to reserve a target antigen exclusively for a specific toxin, then Cyano Biotech’s sellers will receive 10% of that value. A further 10% would be paid from any contract research project associated with the reserving of the antigen and then of any milestone payments. So, to put in context, Simris will need to make EUR 80m in sales from the ADC platform to reach the maximum cap of EUR 8m in earn-outs.

USD 1.9-2.4m implication on valuation per ADC license deal

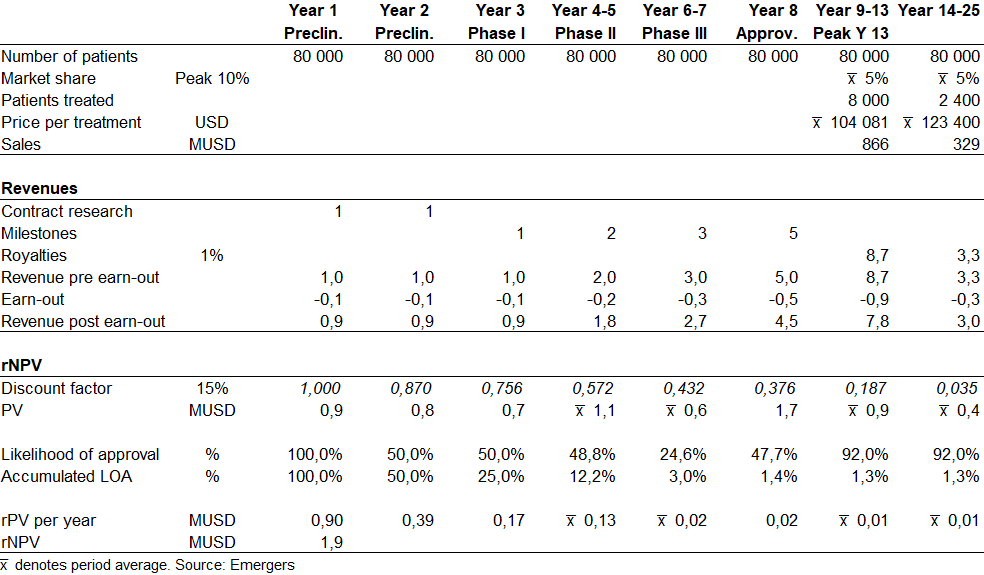

Cyano Biotech has developed and patented a platform technology for the generation and production of novel Antibody Drug Conjugate (ADC) payloads. These are advanced treatments that can couple linkers and monoclonal antibodies (mABs) to proprietary cytotoxins in order to form ADCs that are non-toxic to healthy tissue but lethal to certain tumor cells. The strategy for the ADC platform is to make paid R&D collaboration agreements with pharma companies to jointly develop novel cancer drugs. Beyond payment for the development and optimization of a payload, Simris will receive additional payment at each major milestone e.g., successfully completing pre-clinical development, for the production of the payload in its photobioreactors, and eventually royalties on the sale of any compounds that are market approved and used in the treatment of cancer patients.

To get an idea of what this would mean for Simris we’ve made some broad assumptions. Benchmarked against similar licensing deals, we estimate contract research revenues for the pre-clinical stages of an ADC development project to be around EUR 1m per year, with milestone payments of EUR 1m for entry into phase I, EUR 2m for entry into phase II, EUR 3m for entry into phase III, and another EUR 5m at approval plus a 1-5% royalty fee on sales. Discounted with a WACC of 15% we get the present value (PV) of these future cash flows. We also risk adjust these PVs with the statistical probability of success of each stage of development, based on statistics for oncology development provided by the Biotechnology Innovation Organization for 2011-2020.

Based on an assumption of USD 100,000 per treatment today, 10% peak market share for a cancer indication with 80 000 patients in the 7MM (USA, Japan, France, Italy, UK, Spain, and Germany), this suggests a discounted risk-adjusted rNPV of USD 1.9m (at 1% royalty) to USD 2.4m (at 5% royalty) for each future ADC license deal, after deducting the performance related earn-out to Cyano’s sellers.

With an estimated 4m new shares (EUR 120k in shares paid to Cyano’s sellers at close), we expect this translates to 0,11-0,15 SEK per share.

Adding to the significant revaluation potential

Cyano Biotech has been profitable since 2020, meaning the acquisition is immediately accretive to Simris, and there’s good reason to believe that the patents and advanced discussions with ADC and Pharma companies will enable Simris to accelerate revenue generation in the coming years.

Combined with Simris’ downstream processing capability, we expect the deal to accelerate Simris’ long-awaited entry into the biopharma space. The signs are that this will comprise 1/3 of the business in the next couple of years, alongside the microalgae biomass and food supplements businesses already in scale-up phase. In the longer term, the Cyano vertical has the potential to dominate the business. Supported by only a fraction of listed peer multiples we find support for a fair value of SEK 170m in 2023 and SEK 230m in 2024, noting that each ADC platform license deal might boost potential even further.

DISCLAIMER