Johan Widmark | 2024-06-19 08:00

Building a solid platform for expansion

With the recent announcement that Cindrigo has exited the Slatina 3 geothermal project in Croatia, citing better investment stability and value in Germany, the Company has strategically realigned its portfolio to focus on high-value, lower-risk renewable energy projects across Europe. By prioritizing the 110 MW Waste to Energy plant in Finland and three geothermal projects in Germany, Cindrigo aims to harness immediate revenue potential and scalable growth opportunities.

Kaipola set to generate first revenues in Q4’24

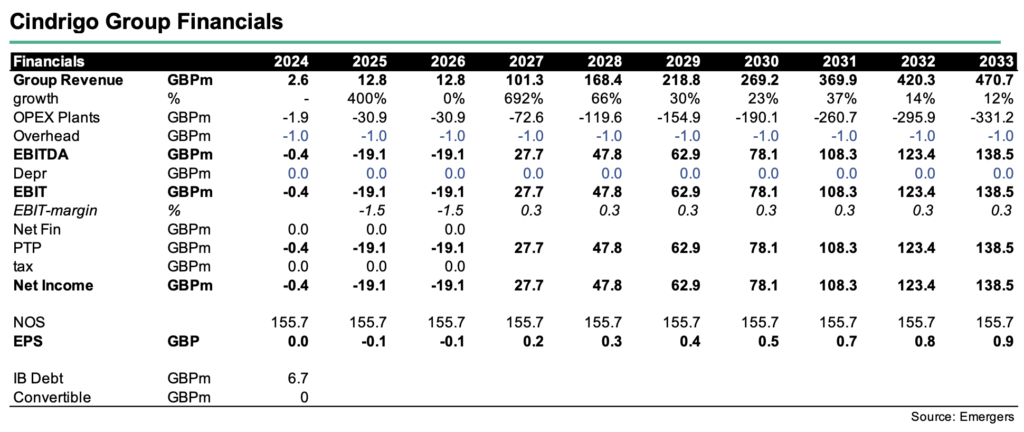

Having closed the acquisition in Finland means Cindrigo has now secured a significant foothold with a 50-year lease on a 110 MW Waste to Energy (WTE) combined heat and power (CHP) plant in Kaipola. With the plant already built, currently undergoing maintenance and upgrades, this will offer revenues already in Q4’2024, with a projection to generate EUR 15 million in its first year of operation, and annual revenues of EUR 40m at full capacity, then contributing EUR 10m in EBITDA.

Remarkable government support for geothermal production

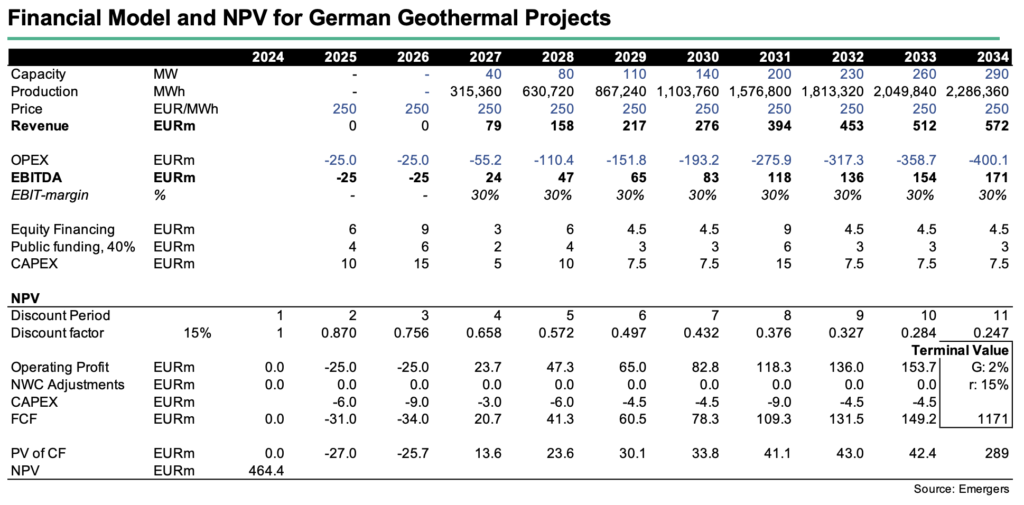

In April, Cindrigo announced the signing of a term sheet with Zukunft Geowärme GmbH to acquire three geothermal energy projects in the Upper Rhine Valley. With an initial target capacity of 80 MW, and a significant expansion potential exceeding 300 MW combined geothermal power and heat, this will give Cindrigo a ca 200MW under contract proving a strong platform for further expansion. Importantly, Germany offers strong government support for geothermal projects with substantial incentives, including a feed-in tariff of EUR 250 / MWh for 20 years and up to 40% federal funding for construction CAPEX. A federal insurance policy is also underway which will essentially eradicate all explorative geothermal drilling risk. This robust support framework positions Cindrigo well to capitalize on Germany’s ambitious target to increase its geothermal heating capacity by 2030.

With the German projects expected to begin generating revenue by Q3/Q4 2027, our NPV shows an Unlevered NPV (15%) of EUR 460m. This however does not take financing or the acquisition cost, which is still undisclosed, into account, and runs a high risk of requiring additional funding to reach its full production potential.

Most but not all pieces in place for a transparent valuation of long-term potential

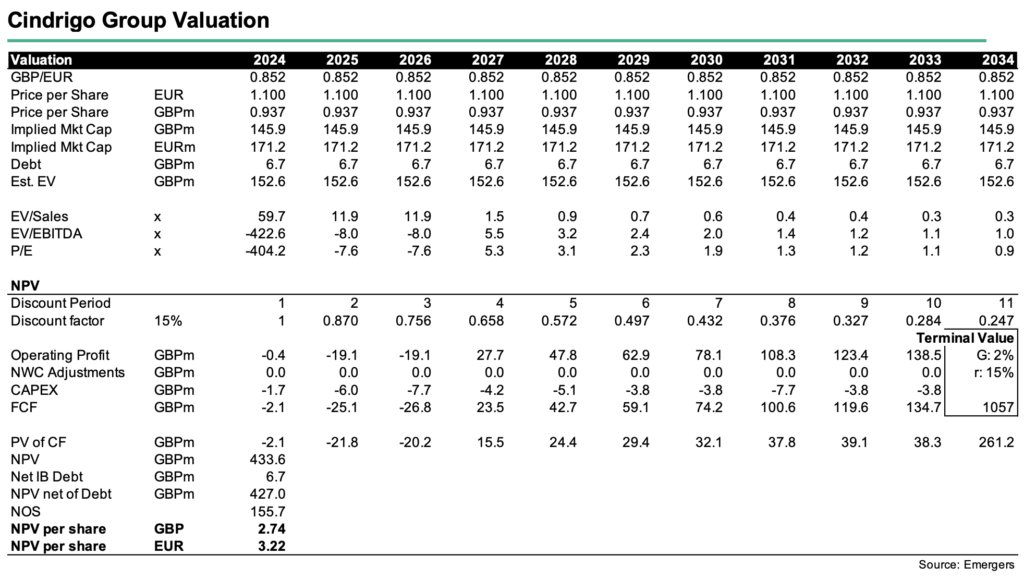

Before any new listing, the most recent data point on valuation is the EUR 1.1 per share at which the payment in shares for Kaipola was made. This implies a Market Cap of GBP 146m / EUR 171m.

Scaling the capacity in Finland and Germany at a linear CAPEX / Production ration and a 15% WACC supports a NPV for the group of GBP 434m. At 155.7m shares after the Kaipola acquisition, this translates to GBP 2.74 / EUR 3.22 per share. This number however needs to be adjusted with the acquisition price for the projects in Germany, which is still undisclosed but should till leave plenty of upside potential in the valuation.

To materialize the Company’s long-term target of 1,000MW we believe that additional external financing will be needed, diluting the Cindrigo shareholders further. The dilution is dependent on how successful the initial rollout is, and how much can be re-invested into new plants.

In our view, the investment case of Cindrigo boils down to how quick, and at what terms new capital can be raised to finance the rollout. Since the company is pursuing a somewhat untouched market with huge growth opportunities, and is run by a management with proven track record, almost all the pieces are in in place for success.

DISCLAIMER

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research does not constitute investment advice and is not a solicitation to buy shares. Information provided here or on Emergers’ website emergers.se is not intended to be financial advice. This research shall not be construed as a recommendation or solicitation to invest in the companies described. Emergers cannot be held liable for either direct or indirect damages caused by decisions made on the basis of information in this analysis. Investors are encouraged to seek additional information as well as consult a financial advisor prior to any investment decision.

This material is not intended to be financial advice. This material has been commissioned by the Company in question and prepared and issued by Emergers, in consideration of a fee payable by the Company. Emergers charges a standard fee for the production and broad dissemination of a detailed note following by regular update notes. Fees are paid upfront in cash without recourse. Emergers may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained herein represent those of the research analyst at Emergers at the time of publication. The company has been given the opportunity to influence factual statements before publication, but forecasts, conclusions and valuation reasoning are Emergers’ own. Forward-looking information or statements contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Emergers shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this material.

No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Emergers’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in this material may not be eligible for sale in all jurisdictions or to certain categories of investors. Investors are encouraged to seek additional information as well as consult a financial advisor prior to any investment decision.

Investment in securities mentioned: Emergers has a restrictive policy relating to personal dealing and conflicts of interest. Emergers does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Emergers may have a position in any or related securities mentioned in this report, subject to Emergers’ policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Incirrata AB (Emergers)

United Kingdom

This document is prepared and provided by Emergers for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the ”FPO”) (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document.

This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States

Emergers relies upon the ”publishers’ exclusion” from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Emergers does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.