Johan Widmark | 2023-03-08 08:00

Offtake and royalty deal with Anglo American

Through its wholly owned subsidiary Dannemora Iron AB, GRANGEX has secured a binding term sheet for an offtake agreement for the planned production of low carbon high-grade iron ore concentrate. With an estimated production period of 11 years and estimated production of 1.0Mt iron ore per year, the deal is worth around SEK 15bn, based on today’s price level. The deal also includes a royalty agreement giving GRANGEX USD 10m upfront (next week) in exchange for a 2% royalty for the future revenues from Dannemora. This effectively secures a material portion of the pre-construction financing for the restart of the Dannemora mine, while also providing a significant stamp of approval to the feasibility of the project.

Strong case for low CO2 iron ore

GRANGEX has now entered the next phase, the construction phase, in producing a world class product with a minimal carbon footprint at Dannemora. It is worth noting that the DFS presented in December 2022 was based on recent quotations and price lists and thereby captured the high inflation during 2022 resulting in SEK 700m higher initial CAPEX (SEK 1.2bn to SEK 1.9bn) as well as 22% higher maintenance CAPEX and OPEX (55 USD/t) compared to the PFS, although this was counteracted by a 17% stronger USD/SEK-rate.

Mix of equity and debt

As the offtake agreement and royalty deal with Anglo American has markedly lowered both the operational and the financial risk in Dannemora, we now apply a 13% (15%) return requirement for equity investors, while maintaining an 8% interest for debt holders, netting a 7.4% WACC in our unlevered DCF approach.

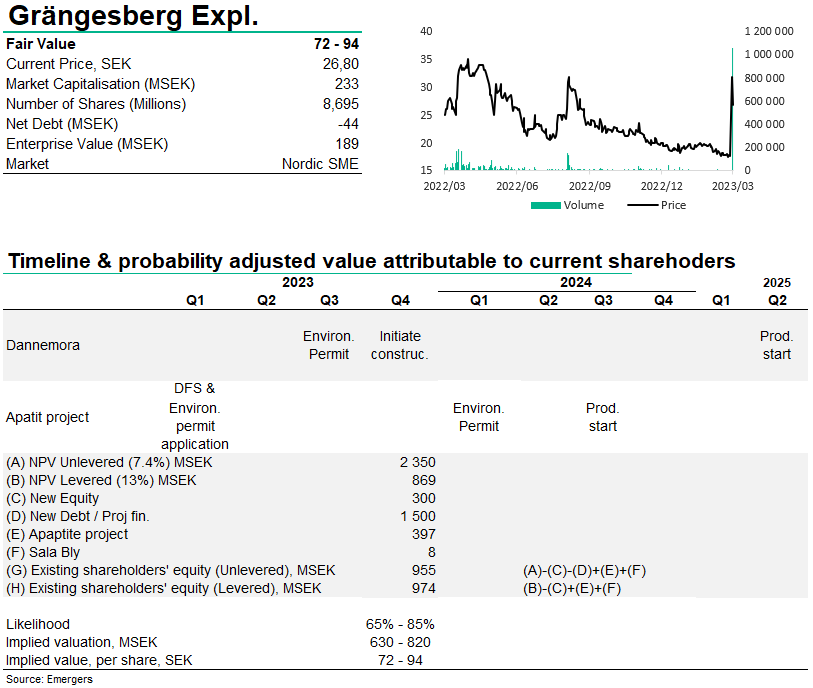

Now we expect the company to raise around SEK 300m from equity investors later this year, along with SEK 1.5bn in a mix of co-investments from strategic investors, project financing and secured debt, most likely involving additional capital from Anglo American. At this point however, it is still difficult to forecast what the final structure will look like, but it will likely affect the Levered Equity Value for GRANGEX’s current shareholders. All in all, we still find support for an Unlevered Net Present Value largely in line with the NPV presented in the company’s DFS.

Significant potential for further revaluation

With a structural long-term growth in demand for green low CO2 iron ore and a prolonged supply crisis following Russia’s cut off from Europe we find a strong fundamental case for both GRANGEX’ projects. We now expect production start for the Apatite project sometime early/mid 2024, Final Investment Decision for Dannemora around winter 2023/24 and production start in H1’25.

We now find support for an Unlevered NPV for Dannemora of SEK 2.3bn after tax. Along with the Apatite project and Sala Bly, and reduced for project financing, this Unlevered approach gives a SEK 955m in Equity Value attributable to current shareholders. Applying a Levered DCF after tax approach, applying only the Cost of Equity (13%) as discount rate, this gives SEK 974m attributable to current shareholders. Using the midpoint of these two numbers and risk adjusted with an estimated probability of successfully of 65-85%, this provides support for a fair value of around SEK 630-820m or SEK 72-94 per share in 12-24m.

DISCLAIMER