The hangover from the pandemic continues to linger for Motion Display. But there are bright spots. With a well-documented effect on sales, a breakthrough order in Australia, progress in Europe, a potential redemptive order in the US and lower OPEX we see a good chance for management to turn the ship around. After some revisions to our model, we now find support for a fair value of SEK 1.6-1.9 (2.1 – 2.5) per share, in 12-24 months.

Andreas Eriksson | 2022-11-25 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

New markets = new opportunities

Motion Display continues to experience headwinds in the US, where the company has put most of its sales effort. While sales in Q3 was soft at SEK 2m, Q4 has gotten off to a better start with two large orders amounting to a total of SEK 3.8m. One bright spot is the entrance to the Australian market with a SEK 1.1m order from global liquor giant Diageo. As Q4 historically has been the strongest quarter, and the two orders in Q4 show how quickly things can change, we´re keeping our FY sales forecast of SEK 18.5m for 2022. The low reported gross margin at 34% in Q3 is a bit worrying, and should be related to rising input costs, but is partly offset by a 23% cut in OPEX relative to Q2´22.Aiming for steady state and beyond

With regards to Motion Display’s technology and product offering our conviction remains strong. Plenty of case studies support a dramatic sales increase in physical stores, and we expect Motion Display to benefit from an increase in in-store marketing spend after two tough pandemic years. Historically, Motion Display has reported sales around SEK 30m in a “normal year”, with a record SEK 50m in 2018. Being somewhat forgotten the company now needs to fight for attention. But the entrance into Australia and recent order in the US suggests that change could be underway.

High-risk case with significant upside potential

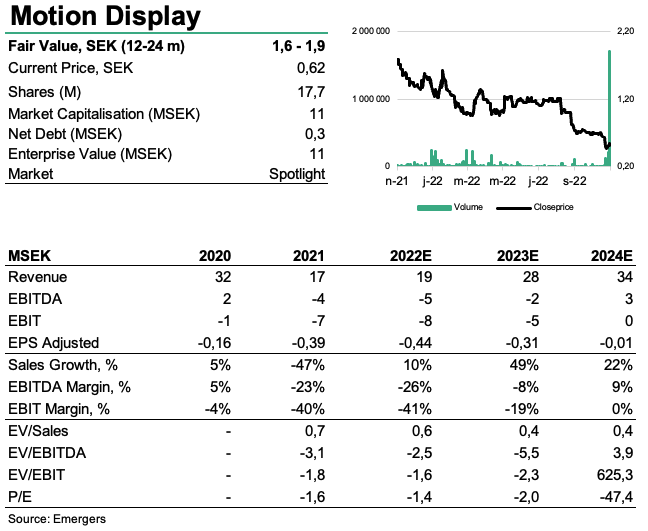

At present, with one-offs orders here and there, we see a somewhat binary investment case, an impression that is further reinforced by the cash position at end of Q3 of a mere SEK 0.5m. While cash has been replenished by a SEK 2m loan from Almi and temporary relief of pre-paid taxes of SEK 3m in Q4, the company needs to increase revenues. We’ve now made some minor revisions to our model, mainly lowering short term gross margins to 35% (45%) as sector colleague Pricer’s margins also took a hit in Q3 following a staggering rise in input costs. We now find support for a fair value range of SEK 1.6 – 1.9 per share (2.1 – 2.5), based on a rather defensive WACC (30%) and conservative target multiples of 1x Sales’24E and 10x EBITDA’24E. Should the company manage to recover to historic revenue levels, which we expect in 2023/24, the depressed sales multiples of 0.5x ‘22E and 0.3x ’24 support a significant revaluation potential in the share.

DISCLAIMER