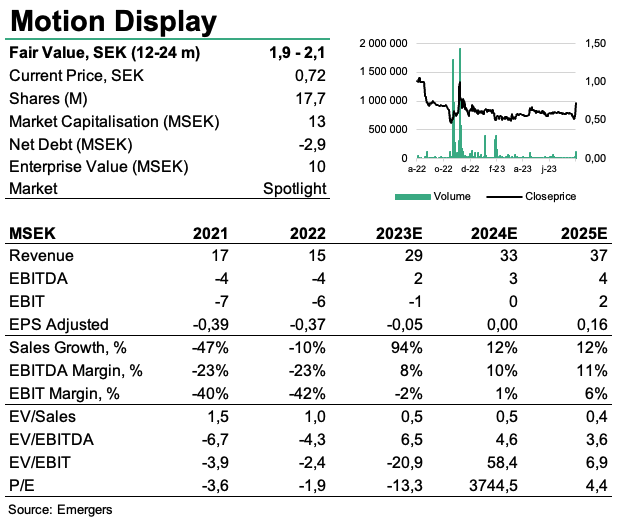

The strong start to 2023 has now made its mark in the books, with the revenues to date already surpassing sales in the full year 2022. With breakthrough orders in several new markets and sales returning to pre-pandemic levels, 2023 appears to be a redemptive year for Motion Display. With a less binary investment case we’ve made changes to our WACC and sales estimates, and now find support of a new fair value range of SEK 1.9 – 2.1 (1.6 – 1.9) per share in 12-24 months.

Andreas Eriksson | 2023-08-29 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Better, stronger, less risky

The figures of H1’23 speaks pretty much for themselves. Sales amounted to SEK 15.2m, resulting in positive EBITDA and cash flow for the first time since 2020. Along with a better geographical spread, Motion Display is on its way back to a new normal, in better shape with tighter cost base and stronger margins. The Q2’23 gross margin reached a record 57%. However, we anticipate a decrease in the margin with even higher volumes. This is because the company’s sales strategy involves partnering with large purchasing organizations, which typically results in lower margins compared to direct customer sales. Even though the recent upswing is due to a recovery in the US, the company has seen traction in other key markets like Europe, Australia and South America. This development is slowly lowering the risks of relying heavily on a single market.Increasing sales with good cost control

The cost efficiency measures implemented in 2022 continue to have a positive impact. Combined with strong gross margins, they set the stage for healthy profitability as sales gradually return to normal. With an annual cost base of approximately SEK 15m and current gross margin of 57%, Motion Display requires sales of around SEK 27m to break even at the EBITDA level. This indicates that the company is on track to achieve profitability (once again) already this year. The last time sales reached SEK 30m (in 2020), Motion Display was valued at SEK 35-40m, or SEK 2.00-2,30 per share. Therefore, the current price of SEK 0.72 represents a significant discount in an historical perspective, especially considering the lower cost base and the higher gross margins.Sales H1’23 > current Market Cap

The reported sales of SEK 15.2m and the backlog of SEK 4.4m for the first six months are good numbers by themselves, but we think what’s behind the figures might be of even bigger importance. Historically, Motion Display was heavily reliant on the US market. However, they struggled to gain consistent traction and often depended on sporadic orders, which made the investment proposition quite unpredictable and binary. We now see the entry into other geographical markets, and better traction in Europe. This diversification reduces investment risk by leading to more consistent orders. We now believe Motion Display finally has a chance to break through the glass ceiling that has been annual sales of SEK 30m on a steady basis. As a result, we’ve made some changes in our estimates and assumptions where a new WACC of 21% (30%), sales of SEK 29m (SEK 23m) in 2023E, a growth rate of 10% (22%) from 2024 and onwards now support a fair value range of SEK 1.9 – 2.1 per share in 12-24 months.

DISCLAIMER