Johan Widmark | 2022-08-18 08:00

Acquisition to accelerate entry into BioPharma

Cyanobacteria are a member of the microalgae family, and are best cultivated in photobioreactors, just as used by Simris since establishment. With the LOI to acquire German cyanobacteria firm Cyano Biotech GmbH, Simris aims to gain an inhouse R&D capability that includes a commercial stage platform solution for antibody-drug conjugation (ADC). These are advanced treatments that can couple linkers and monoclonal antibodies (mABs) to proprietary cytotoxins in order to form ADCs that are non-toxic to healthy tissue but lethal to certain tumor cells. Cyano, which brings with it deep scientific competence and arguably the world’s larget library of cyanobacteria producer strains, has very limited production capacity – something that Simris has plenty of – and hence the immediate synergy. Cyano’s research IP includes a platform to create novel, optimised ADC payloads and a global patent for microcystins as a payload that offers to unlock further value.

The terms of the takeover are not yet announced but considering that Cyano Biotech had an average turnover of EUR 0.5m and an EBITDA of EUR 114k in the past two years, it is likely that performance related payments will be a large part of the deal, in addition to cash and Simris shares.

High activity over summer, but less so on the revenue side

Along with the LOI, Simris also presented its report for Q2’22. In the quarter, Simris saw a significant reduction in both revenues and expenses, with a net improvement of the EBITDA loss to 4 MSEK in Q2’22. During summer Simris has prioritized upgrading the production facility over production of biomass, which is a process that will continue into 2023 with the aim of gaining the GMP certification within the next two years, a certification that is necessary to operate in the BioPharma industry.

Importantly, Simris has presented an outline of the revenue generation for the near term (H2’22), mid-term (2023) and long-term (2024 and beyond) and broken these down into B2B and B2C. While leaving out exact numbers, this gives a good insight into the strategic roadmap, where Simris expect a rebound in B2B biomass sales by 2023, a re-launch of the Omega 3 supplements targeting the B2C market in the US and Europe in H2’22 and 2023, and BioPharma partnerships in 2024. These partnerships will generate revenue in the form of contract research, milestone payments, and ultimately royalty payments.

ADCs a high margin application of Simris photobioreactor

Over the past decade, ADC has quickly caught up to promising and highly advanced immunotherapies such as CAR-T, and is now amongst the fastest growing drug classes in oncology. Instead of extracting T cells and reengineering them to scan and attack cancer cells, ADC therapy applies mABs to locate specific cancer cells and then deliver chemotherapeutic drugs to destroy them. In an ADC, the antibody and the toxic payload are connected by a linker, which ensures that the chemical drug won’t be released unexpectedly before reaching to the antibody target antigen, thus avoiding off-tumor toxicity.

With a price of ADC treatments available today (12 approved by the FDA so far) of around 100 000 USD per treatment, they are less expensive then CAR-T at around 500 000 USD per treatment.

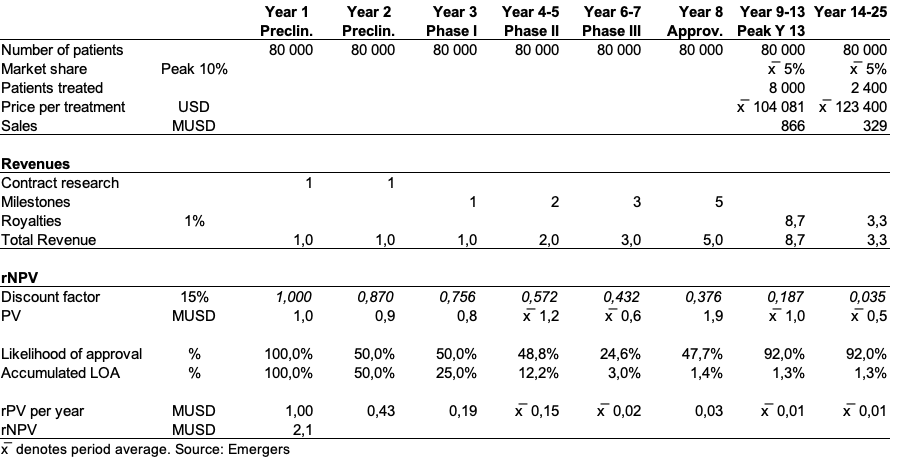

Implications on valuation USD 2.1-2.7m per ADC license deal

From our understanding of what Cyano would bring to the table, we see a good opportunity for synergies where the combined companies would create an ADC platform offering that would license out its technology to pharma companies on a per project basis.

To get an idea of what this would mean for Simris we can make some very rough assumptions. Guided by similar licensing deals, we estimate contract research revenues for the pre-clinical stages of an ADC development project of EUR 1m per year, milestone payments of EUR 1m for entry into phase I, EUR 2m for entry into phase II, EUR 3m for entry into phase III, another EUR 5m at approval and a 1-5% royalty fee on sales. Discounted with a WACC of 15% we get the present value (PV) of these future cash flows. We also risk adjust these PVs with the statistical probability of success of each stage of development, based on statistics for oncology development provided by the Biotechnology Innovation Organization for 2011-2020.

Based on an assumption of USD 100 000 per treatment today, 10% peak market share for an cancer indication with 80 000 patients in the 7MM, this suggests a discounted risk-adjusted rNPV of 2,1 MUSD (at 1% royalty) to 2,7 MUSD (at 5% royalty) for each future ADC license deal, before any performance related cuts to Cyano’s sellers.

rNPV model for unspecified ADC project

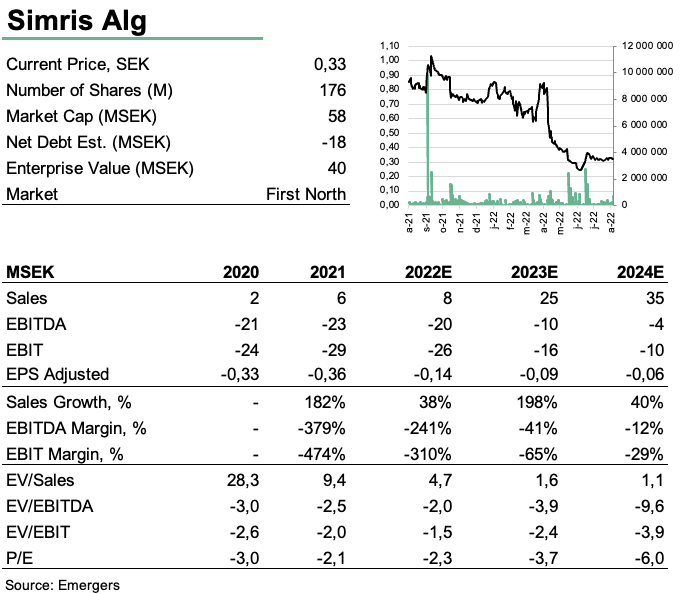

Lower estimate for 2022, awaits close to include Cyano

All in all, we find a lumpiness in operating revenues paired with an acceleration in development, both in terms of R&D and infrastructural upgrades, that pushes our revenue forecast somewhat into the future. As a consequence we have lowered our Sales forecast for 2022. The targeted acquisition of Cyano is however a very interesting strategic fit, and combined with Simris’ downstream processing capability, we expect the deal to accelerate Simris’ long awaited entry into the biopharma space, grow into 1/3 of the business in the next couple of years, alongside the algae biomass and food supplements businesses already in scale-up phase, with potential to dominate the business long-term.

For now however, we do not include Cyano in our numbers but continue to see an upside risk to our forecast of 25 MSEK in sales in 2023 and 35 MSEK in 2024 with a positive EBITDA by 2025. Supported by only a fraction of listed peer multiples we find support for a fair value of 150 MSEK in 2023 and 210 MSEK in 2024, which translates to 0.85 SEK and 1.19 SEK per share in 2023 and 2024 respectively.

Read more about Simris Alg here

Fourth fucoxanthin order confirms commercial turnaround and sets Simris up for revaluation in 2022

With four orders with a total value of 7.5 MSEK in the last eight months, of which two booked in the first two months of 2022, it is

DISCLAIMER