Johan Widmark | 2026-05-13 08:00

Executive Summary

Following its listing on the LSE Main Market in October 2025, Cindrigo has now moved into an execution phase supported by a materially strengthened funding position and a broadened industrial scope. The recently announced funding package comprises GBP 6.7m in new equity at 12 pence per share, alongside up to GBP 2m in additional committed capital and EUR 3m directed into the Fuelwood Finland joint venture, implying total funding and guarantees exceeding GBP 11m. The investment was secured at a premium to recent trading levels, signaling improved investor confidence while extending financial runway. At the same time, the launch of Fuelwood introduces a new high-potential biomass product line, expanding Cindrigo’s role from energy producer to an integrated biomass platform including heat, power and pellets.

In Finland, the integration of pellet production alongside the Kaipola CHP plant implies a slower near-term ramp-up than previously anticipated, but with a significantly enhanced long-term earnings profile. Fuelwood is expected to reach an initial production run-rate of ~80,000 tonnes annually during 2026, scaling towards ~400,000 tonnes, corresponding to revenue potential of GBP 20m in the near term and up to GBP 100m at full capacity based on current prices of GBP 240/tonne. In addition, Cindrigo will generate recurring management service revenues of EUR 75k per month (EUR 1m annually), while the pellet facility becomes the primary off-taker of 30–50MW of heat at EUR 70/MWh, above prior assumptions. The integrated structure reduces reliance on third-party customers and supports a combined business with targeted margins of around 30% at full scale (including ~50MW heat, ~15MW power and pellet output), albeit with full ramp now expected closer to 2029.

In Germany, Cindrigo continues to advance its geothermal portfolio, where recent developments further improve the project risk-reward balance. The strategy centres on its 85%-owned portfolio in the Upper Rhine Valley, comprising three licences targeting around 300MW of combined heat, power and lithium production over the next decade. This positions Cindrigo to capitalise on Europe’s elevated energy prices, decarbonisation and energy security trends, supporting potential group EBITDA of over EUR 90m by 2030, including an initial >EUR 10m contribution from lithium. The project structure remains highly attractive, with the Kaishan partnership deferring 70% of on-surface EPC costs until six months after commercial operation, complemented by substantial public support including a 50% subsidy on pre-drilling costs, 30–40% CAPEX subsidies for heat infrastructure, government-backed project financing and a 20-year power off-take tariff of EUR 250/MWh.

In addition, state-backed drilling insurance combined with Munich Re coverage materially reduces exploration risk by securing up to 90% of drilling capital, while successful wells unlock access to approx. EUR 25m in soft loans and require only around EUR 10m in upfront equity to support a EUR 30m plant build. At the same time, revised assumptions for lithium extraction, requiring approximately EUR 5m in additional CAPEX, indicate recoverable volumes of around 2,500 tonnes of lithium carbonate equivalent (after conversion), with an assumed realized price of EUR 11,000 per tonne.

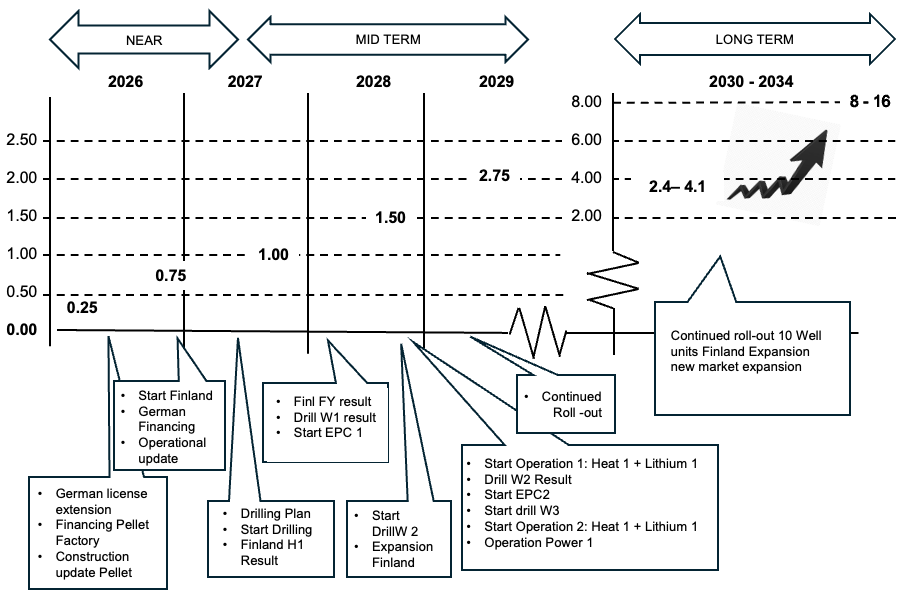

In our revised model, taking the 17% dilution from the recent raise into account, we now find support for a risk-adjusted near-term valuation of around GBP 0.25-0.50 per share (underpinned by the new strategic investor’s willingness to invest at GBP 0.12). With the startup of the pellets production we find support for a stepwise revaluation (only illustrative, intended to show the potential valuation effect of successful de-risking initiatives) towards 0.75 by the end of 2026, GBP 1.00 in 2027 with a longer-term upside supported by potential EBITDA of >EUR 90m by 2030 and a peer-based multiple valuation of around GBP 2.4-4.1 per share. In a longer-term perspective to 2034, we continue to find that growth, structure and profitability improvements could support a share price in the GBP 8–16 range.

Illustration of Key Risk Reduction and Value Creation Events

Fair Value Potential, GBP/Share

DISCLAIMER