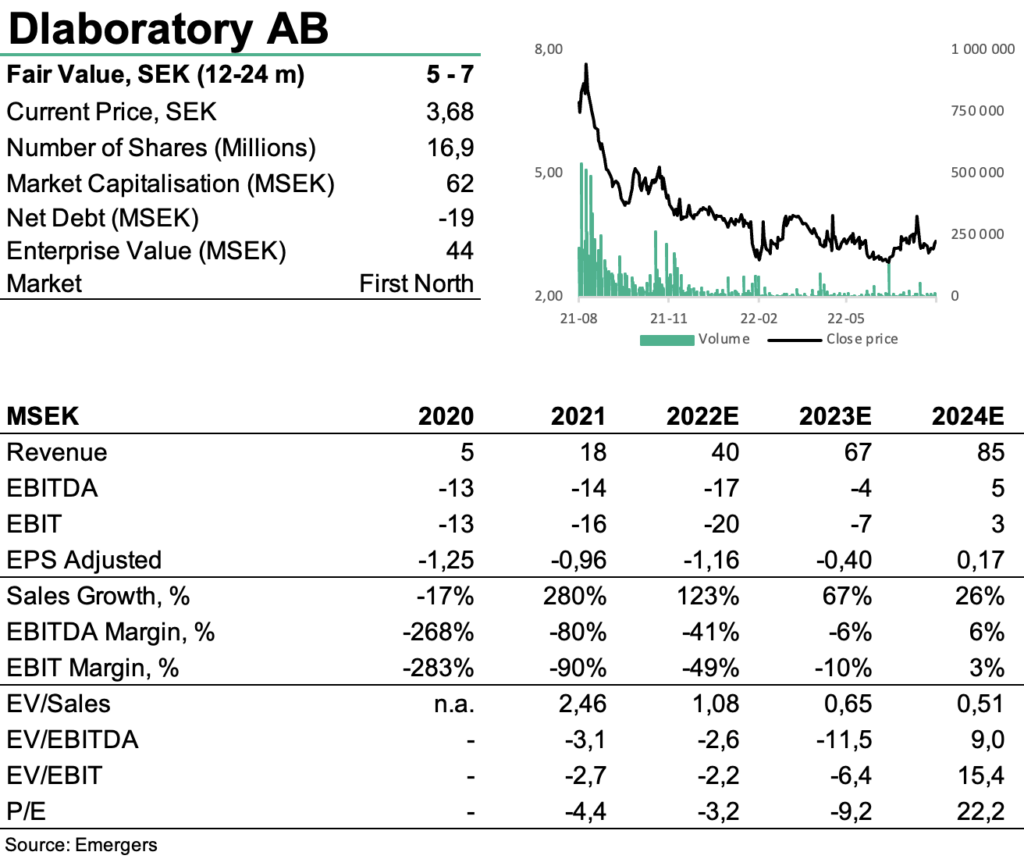

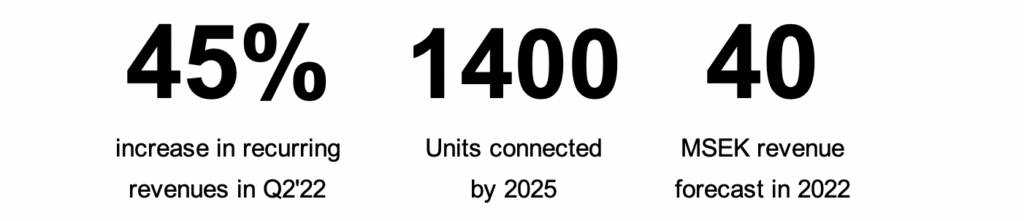

The rise of network stability and electricity security on the public agenda has finally started to translate into a material rise in interest for Dlab’s services. While we note record sales in Q2’22, several new orders and expansions with existing customers, a 45% increase in recurring revenues in the quarter, as well as a new international customer in Dubai, the lower than expected contribution from SLB motivates a slight revision of our forecast for 2022. All in all, we find support for a fair value of SEK 5-7 (7-9) per share on a 12-24 month horizon, but also note that a breakthrough in the international roll-out holds potential for business in the hundreds of millions, which can change the valuation significantly.

Johan Widmark | 2022-08-26 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Several new deals

The encouraging news flow seen in the report for Q1’22 accelerated in Q2’22, with deals with E.ON and another three domestic network companies, a first customer for the new analysis service dServices, as well as a customer in Dubai, the Dubai Electricity and Water Authority. This was followed by an order of advances status control for 500 network stations for Vattenfall and six new orders from existing customers after the end of Q2. With deliveries of both the IT-platform and grid inspections expected in H2’22, along with an increased focus on grid stability in Sweden as we approach winter, we expect the strong business momentum to carry on well into 2023 and beyond.

Downwards forecast adjustment amidst positive momentum

Since the “decreasing telecom network inspections and resource allocation for deferred new business (Corona measurement)” in H1’22 resulted in a lower contribution from SLB than we had expected, we have made a downwards adjustment of our revenue forecast for FY’22 to SEK 40m. Seeing also that the international roll-out is somewhat slower to scale and with longer lead times that expected, we have also lowered our growth assumptions for the IT-platform in Dlab, and now expect the group to pass the SEK 100m revenue mark in 2025E rather than in 2023E. Cash amounted to SEK 20m at end of Q2’22, which implies runway of another 4-5 quarters of current burn rate. Considering that the TO1 has a subscription price of SEK 11,1, we don’t expect that to bring in any new cash in September.

Strong underlying trend support high long term potential

In September 2022, Erik Severin will step down as CEO to be replaced by Rickard Jacobson, coming from the role as CEO of Comsys. We continue to see a chance for 600 units connected in the domestic markets and 800 units connected outside the domestic markets by the end of 2025, which would translate into recurring revenues of SEK 80 million per year. This is supported by a strong trend in network investments among Swedish power utilities, up 15% in 2021. However, Dlaboratory continues to be affected by the general low risk appetite for tech development companies with profits far into the future. All in all, we now find support for a fair value of SEK 5-7 (7-9) SEK on a 12–24-month horizon, at a medium to high risk in Dlab, where the most significant risks consist of long lead times and high thresholds for adaptation.

DISCLAIMER