GRÄNGESBERG EXPLORATION With the Definitive Feasibility Study (DFS) for Dannemora and the appointment of financial advisors to implement a two-phased funding structure, GRANGEX now enters the next, construction phase in Dannemora. With a strong case to produce high-grade (+68%) iron ore concentrate with low carbon footprint, Dannemora meets the profile demanded by producers of green steel.

While the inflationary environment has a meaningful impact on projected costs, this is offset by longer production period (11y) and a 17% strengthening of the USD/SEK, compared to the PFS. Combined with a recent 24% increase in mineral reserves for the Apatite project, a 700 MSEK hike in required financing and a revised financing structure, we find support for a risk-adjusted fair value of 47-61 (98-168) SEK per share in 12-24m.

Johan Widmark | 2023-01-16 12:00

Strong case for CO2 free iron ore, albeit at higher cost

In the announcement of the DFS, GRANGX shows that a world class product can be feasibly produced with a minimal carbon footprint at Dannemora for a longer period compared to what was presented in the Pre-Feasibility Study (PFS). The DFS is also based on recent quotations and price lists and thereby captures the high inflation in 2022 resulting in 700 MSEK higher initial CAPEX (1.2 BN SEK to 1.9 BN SEK) as well as 22% higher maintenance CAPEX and OPEX, although this is offset by the 17% stronger USD/SEK-rate.

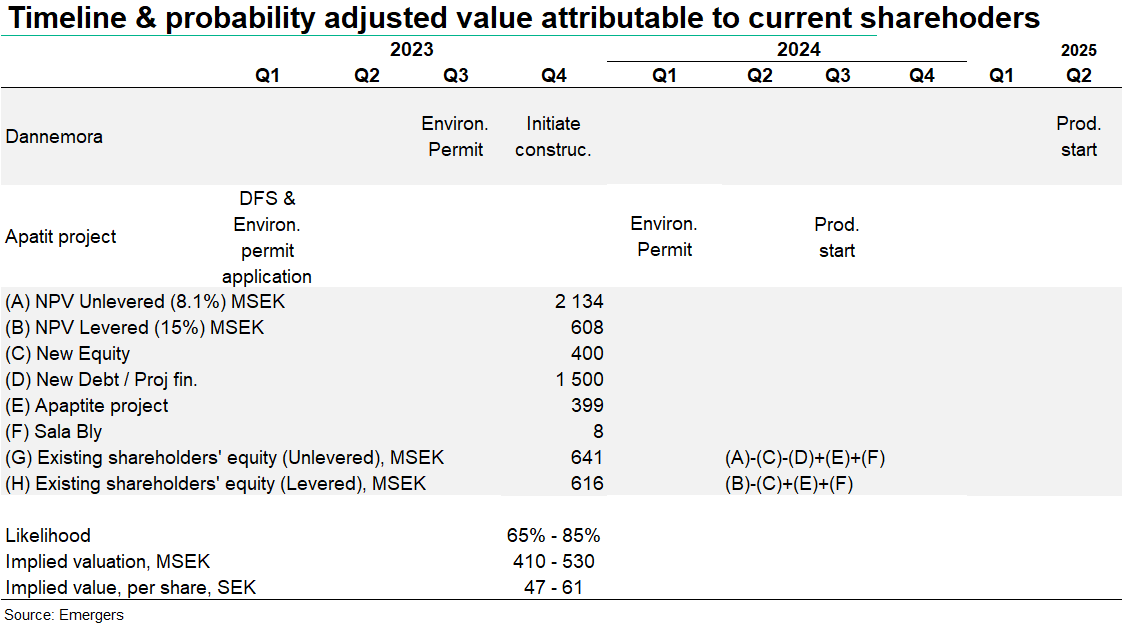

All in all, this gives Dannemora an Unlevered Net Present Value Pre-tax of 2.9 BN SEK in the company’s model (in line with the NPV in the PFS) which is based on 8% discount rate. With the appointment of financial advisors (Swedbank AB and SpareBank 1 Markets AS) the company now plans for a two phased capitalisation.

Mix of equity and debt

In our previous model we estimated 50% debt financing at 8% interest and 50% new equity with a return requirement at 15%, netting a WACC at 11.5%. Now we expect a smaller round of 400 MSEK in H1’23 to fund the planned CAPEX for 2023, and then a larger round around winter 2023/24 for the remaining 1.5 BN SEK. While these two rounds will probably involve a mix of co-investments from strategic investors, project financing with secured debt and equity, it is still difficult to forecast what the final structure will look like. But this will affect the Levered Equity Value for GRANGEX’s current shareholders.

Bullish outlook for Dannemora’s product

Considering that high-quality >67% Fe concentrate will be essential to facilitate the green transition, while only ~4% of global iron ore production is of >67% Fe grade, this will command a price premium compared to 62% and 65% Fe grade. And with the high-grade iron ore market segment expected to grow at an 8% CAGR, from 110Mt today to 750Mt in 2050, this premium is likely to expand in future.

Upwards reserve revision of the Apatite project

Earlier in December, GRANGX also announced an increase of the mineral reserves in the Apatite project, by 24% to 3.5 Mt after tests of the under-water part of the tailings in the JanMatts dam. This will likely extend the production period from 2028/29 into 2031. The apatite project in Grängesberg is a recycling project where the old tailings from the iron ore production at the closed Grängesberg mine will be recycled to produce highly enriched apatite. Next step for the Apatite project is the DFS and environmental permit application, which we now expect in Q1’23.

As for prices, the prolonged war in Ukraine and subsequent trade restrictions have resulted in an extension of the price peak in phosphate rock, with prices now parked north of 300 USD/t. For our valuation model however, we only include a small portion of this for the Apatite project.

Significant revaluation potential despite surge in costs

With a structural long-term growth in demand for green CO2 free iron ore and a prolonged supply crisis following Russia’s cut off from Europe we find both a strong fundamental case as well as a bright backdrop for the projects. We now expect production start for the Apatite project sometime early/mid 2024, Final Investment Decision for Dannemora around winter 2023/24 and production start in H1’25.

Guided by GRANGEX’ Company Presentation, we now expect a debt/equity raise in H1’23 totaling 400 MSEK, and another 1.5 BN SEK in winter 2023/24, of which we expect majority to be project financing/debt. Assuming 15% cost of Equity and 8% Cost of Debt this gives a discount rate of 8.1% after tax (roughly in line with company discount rate at 8%).

However, the higher upstart CAPEX for Dannemora increases our estimated upfront financing need from 1.3 BN SEK to 1.9 BN SEK. Along with a projected realised selling price (FOB) of 129 USD/t and OPEX at 55 USD/t we find support for an Unlevered NPV for Dannemora of 2.1 BN SEK after tax and a 27% IRR. Along with the Apatite project and Sala Bly, and reduced for project financing, this Unlevered approach gives a 641 MSEK in Equity Value attributable to current shareholders.

Applying a Levered DCF after tax approach, applying only the Cost of Equity (15%) as discount rate, this gives 616 MSEK attributable to current shareholders. Using the midpoint of these two numbers and risk adjusted with an estimated probability of successfully of 65-85%, this provides support for a fair value of around 410-530 MSEK or 47-61 (98-168) SEK per share in 12-24m.

DISCLAIMER

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research does not constitute investment advice and is not a solicitation to buy shares. Information provided here or on Emergers’ website emergers.se is not intended to be financial advice. This research shall not be construed as a recommendation or solicitation to invest in the companies described. Emergers cannot be held liable for either direct or indirect damages caused by decisions made on the basis of information in this analysis. Investors are encouraged to seek additional information as well as consult a financial advisor prior to any investment decision.

This material is not intended to be financial advice. This material has been commissioned by the Company in question and prepared and issued by Emergers, in consideration of a fee payable by the Company. Emergers charges a standard fee for the production and broad dissemination of a detailed note following by regular update notes. Fees are paid upfront in cash without recourse. Emergers may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services.

Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained herein represent those of the research analyst at Emergers at the time of publication. The company has been given the opportunity to influence factual statements before publication, but forecasts, conclusions and valuation reasoning are Emergers’ own. Forward-looking information or statements contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations.

Exclusion of Liability: To the fullest extent allowed by law, Emergers shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this material.

No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Emergers’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in this material may not be eligible for sale in all jurisdictions or to certain categories of investors. Investors are encouraged to seek additional information as well as consult a financial advisor prior to any investment decision.

Investment in securities mentioned: Emergers has a restrictive policy relating to personal dealing and conflicts of interest. Emergers does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Emergers may have a position in any or related securities mentioned in this report, subject to Emergers’ policies on personal dealing and conflicts of interest.

Copyright: Copyright 2023 Incirrata AB (Emergers)

United Kingdom

This document is prepared and provided by Emergers for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the ”FPO”) (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document.

This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States

Emergers relies upon the ”publishers’ exclusion” from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Emergers does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.