Research: Johan Widmark | Date: April 7, 2021

IMU the main driver in KebNi’s revamp

The appointment of new CEO Torbjorn Saxmo in February should mean an increased focus on sales and new sales channels for Maritime and IMU. While Maritime’s products have achieved competitive maturity, COTP and IMU will require investments to nibble away the tech debt during 2021. While the SAAB contract can be expected to reach SEK 40 million within a few years, an essential development of the IMU portfolio is expected to result in a broader and more competitive range of products covering unit sales, solutions and at least one, yet to be announced, application, while it also opens the door for new potential high-volume customers.

Interesting opportunities behind strategic question marks

The COTP Land business, which today accounts for two-thirds of revenues, should benefit from good underlying market growth for VSAT, and with a freshen-up it should be possible to reduce dependence on the Russian market. In addition to fundamental uncertainties for COTM Land, basic strategic issues remain unresolved, such as recurring revenue from software/service and migration from box delivery to solutions provider, which also present interesting opportunities for KebNi.

Plenty of upside potential if sentiment can be turned

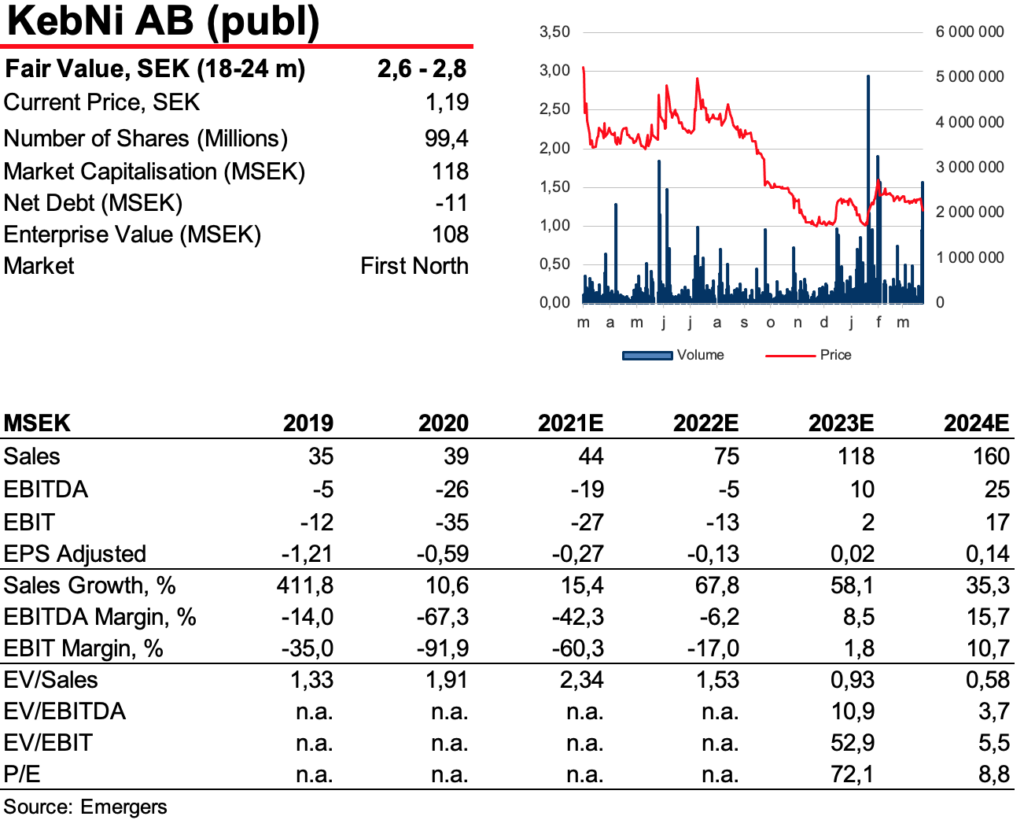

The stock is under pressure from low confidence and a high proportion of shares (69%) in the hands of the guarantors following the rights issue in 2020. Since the acquisition that accounts for most of the revenue was made about a year ago, historical figures provide limited guidance and make the cost side particularly difficult to estimate. If KebNi succeeds in defending a gross margin of +40% for large new contracts (compared with our estimates for IAI <30% and IMU 35%), we expect cash flow breakeven at sales of approximately SEK 90 million. We see a fair value of SEK 2.6-2.8 per share on a 24-month horizon in our base case, using target multiples and DCF (12% WACC), with the support of the capital injection of SEK 38 million and the new management’s strategic direction.

Company description

KebNi AB (publ.), formerly ASTG AB until July 2020, is active in technology, products and solutions for security, positioning and stabilisation. The company has extensive experience in solutions for maritime satellite antennas and inertial sensor systems for motion detection.

The company currently has operations in two different product areas: satellite antenna platforms and inertial motion sensors (IMUs).

Satellite antenna platforms include the following activities:

- KebNi Maritime – innovative 4-axis stabilized VSAT terminals for primarily maritime installations.

- KebNi Land Mobile, which consists of two arms

- KebNi Comms on the Move (COTM Land) – stabilized mobile antennas for vehicles traveling or moving over land.

- Satmission by KebNi – Comms on the Pause (COTP Land) – Driveaway antennas where the vehicle stands still upon satellite contact.

- KebNi Inertial Sensing (inertial measurement units, IMUs) – advanced inertial sensor systems for measuring movement in three dimensions. IMUs are a key component in the company’s stabilized satellite platforms and are also sold to external customers for other applications.

In 2020, KebNi acquired technology from ReQuTech AB in COTM Land, and Satmission AB in COTP Land as a complement to its existing product portfolio.

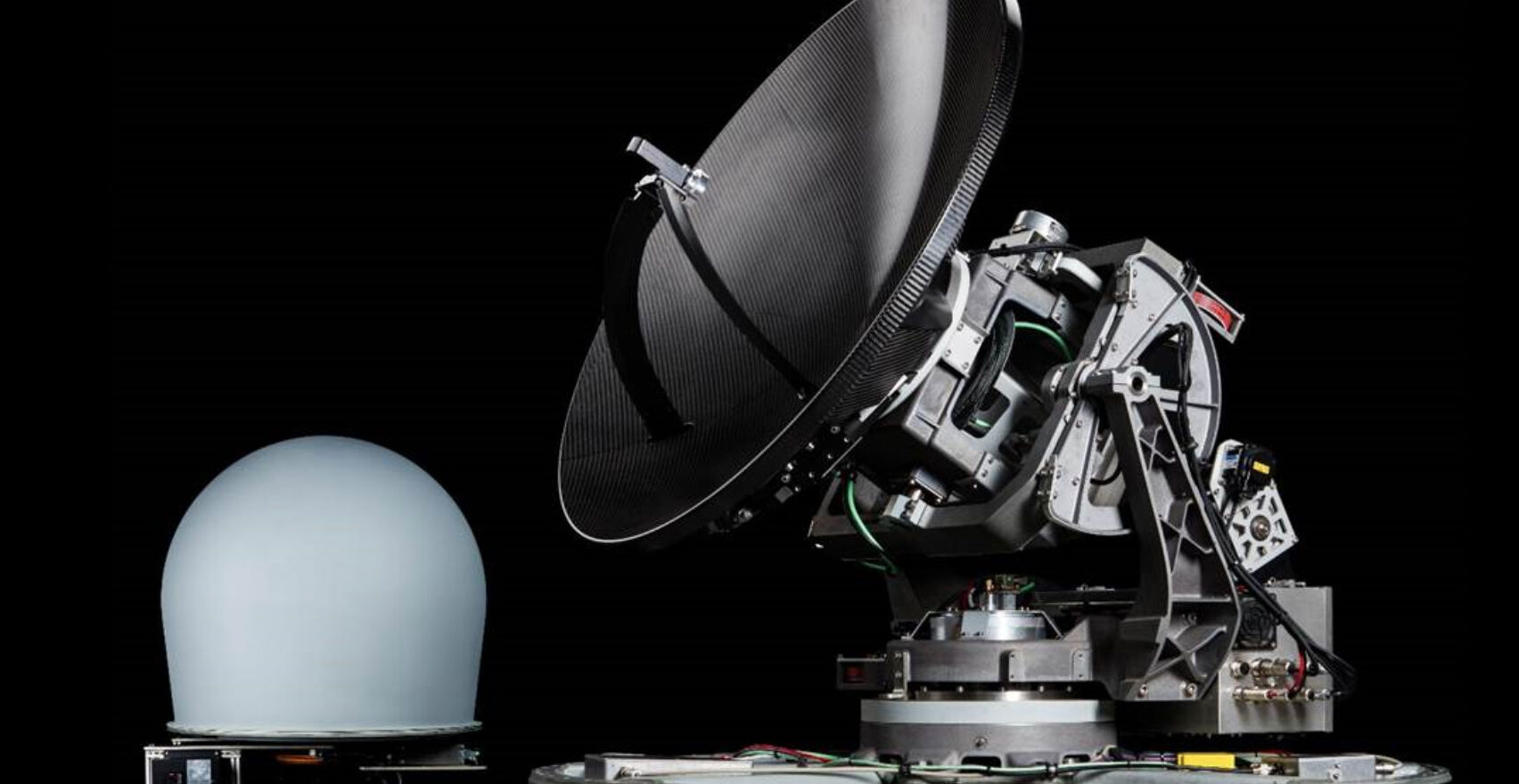

Maritime – the historical core of the company

Market and operations

The market for stabilized VSAT terminals for marine applications is mature and characterized by large price differences between simpler antennas for commercial use and the advanced antennas used on coastguard and military vessels. Provision of VSAT terminals often takes place in collaboration with System Integrators the deliver turn-key systems.

There are only a handful of military system suppliers providing the majority of advanced VSAT terminal systems for the military maritime market. These suppliers include well-known names like General Dynamics (USA), ORBIT (Israel) and EM Solutions (Australia). The focus in this field is on technical performance, and the price levels are significantly higher than in the commercial market. In terms of numbers, the global market is estimated to amount to about 1,000 units per year.

In the early 2000s, the then C2SAT developed platforms for VSAT antennas for maritime use. The early P7 (Platform 7) stabilization system was sold to commercial shipping companies and cruise ships. An estimated one hundred units were sold from the mid-2000s until 2012. In December 2012, discussions were initiated with Israeli company IAI, which resulted in the launch of a development project for P9 to meet much tougher specifications and military requirements. Deliveries of this version began in 2019, and KebNi has so far delivered units for about SEK 60 million with this military certification. This is the segment’s main focus today.

Forecasts

Given its relationship with IAI, KebNi can be expected to continue to receive add-on orders, but the real potential of this business lies in reaching new major customers in the military segment. However, the sales cycles are long, at 12-36 months. One important sales channel is to become included in the ”internal product catalogues” of major system integrators such as Airbus and Thales, which could shorten lead times for contracts and offer larger volumes. We believe the company is well placed to achieve this position with at least one major player that has strong relationships with end customers globally, but nothing has been confirmed yet.

Furthermore, the experience of new CEO Torbjorn Saxmo from SAAB, who has an extensive track record of selling to the kind of customer that KebNi Maritime addresses, could open up new sales channels for KebNi. Given an anticipated strengthening of the sales force, we see 2021 as an intermediate year in terms of sales but we are upbeat about the long-term outlook for Maritime.

A realistic near-term ambition is to deliver 20 units per year, but we see potential to grow to 50-100 units (corresponding to a global market share of 5-10%) in the longer term.

Prices are difficult to estimate and vary greatly depending on configuration and composition. We estimate that antenna prices in deliveries to IAI are lower than the expected price of future deliveries to new customers, and that they cover production costs but not development costs. In order to have full cost coverage and a healthy gross margin of 40-50%, the company would need to raise the prices for future contracts to almost double.

We also expect that the company will eventually be able to introduce some form of as-yet-unknown recurring revenue in the form of service, support or licence agreements (see Strategic Issues below).

Land Mobile – COTP (Communication on the Pause)

Market and operations

The market for COTP Land antennas is growing steadily. The company estimates that there are approximately 8–10 significant competitors globally, with KebNi’s recently acquired Satmission as an established brand in the industry with operations since 2004.

KebNi’s operations within COTP Land are based on the acquisition of Satmission in May 2020. New applications are being developed in the same area as COTM Land, and KebNi will position the two businesses together for a more complete solution offering. The products are aimed at the high-quality segment with commercial and public-sector customers. To date, Satmission has delivered over 300 antennas and has sales in 10 countries and over 10 distribution channels. That said, the company is assumed to have a high exposure to the Russian market.

The company currently offers three antenna sizes ranging from 1.25 m to 1.75 m, with a price range estimated at one-fifth of KebNi’s maritime products, depending on the configuration. However, documentation and other matters have been neglected in recent years and KebNi is now investing to freshen up the portfolio during 2021.

Forecasts

After a refresh during 2021, we expect COTP Land to be able to grow more than the market’s annual 13%. Once again, we expect that over time the company will be able to introduce some form of recurring revenue in the form of service, support or licence agreements.

Land Mobile – COTM (Communication on the Move)

Market and operations

The market for COTM Land antennas is growing. Solutions for advanced military applications are offered by the same suppliers as for COTP Land. KebNi estimates that segments with limited budgets such as police, ambulance and rescue services plus commercial and military segments have a greater need for higher-performance antennas intended for use on the move and that address specific applications. The competition in this segment consists of approximately eight to ten suppliers globally.

An initial demonstrator version with basic functionality is expected to be ready in the spring. Once the demonstrator version is ready, it will be used to estimate demand from different customer segments, and any willingness to co-finance further development.

The spontaneous idea of fitting a maritime COTM Land antenna to a land vehicle in motion does not work, partly because the movements are different and partly the size and shape are wrong. The shape needs to be flatter, and it is likely that the development in this segment will move towards flat panel/phased array (see Strategic Issues below).

Forecasts

Our base case assumes the company will not identify a party interested in co-financing the COTM Land product to suit public-sector or military customers, and that it instead allows the product to continue as an adjunct to COTP Land with sales of a few individual units per year.

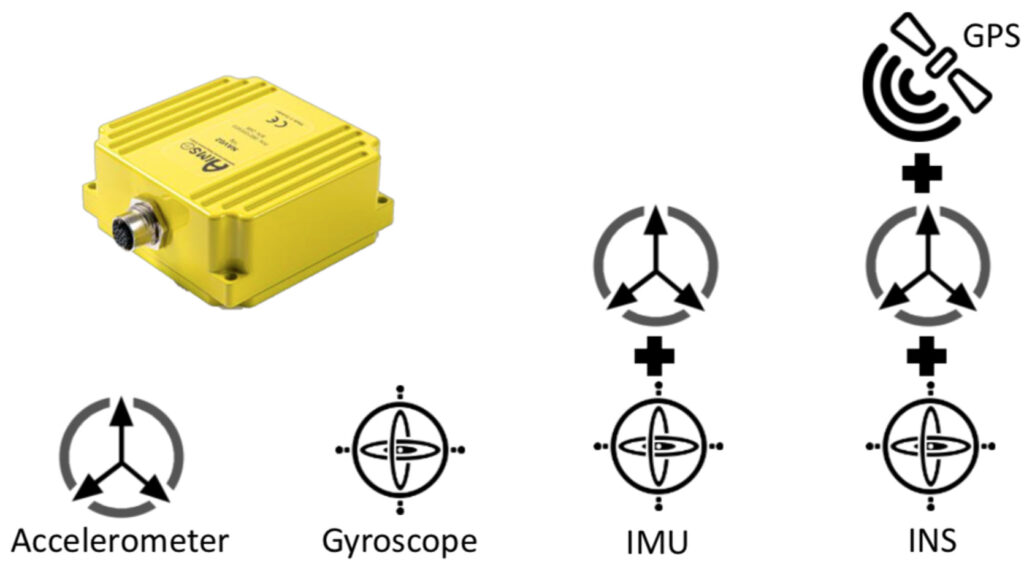

Inertial Sensing (IMUs)

Market and operations

The market for inertial sensors has a large number of suppliers (50+), distributed between market segments, with each segment defined by performance requirements, costs and size. Solutions are usually customized and optimized for a specific application.

The existing market players include Honeywell and Northrup Grumman. The military segment includes Atlantic Inertial Systems (AIS), which was previously part of BAE Systems and is now owned by UTC. There are a number of players in the commercial segment, such as Xsense, SBG Systems and VectorNav.

The development of KebNi’s IMUs has been neglected, and the company expects to invest during 2021 to raise its technology to the forefront. KebNi’s goal is for the new IMU to be able to be used in a wide range of applications, have high performance and a small size at a very competitive price. The IMU will be offered with a fully integrated GNSS receiver and advanced sensor fusion to provide robust and reliable data for position, speed, and orientation under demanding conditions.

One of KebNi’s main strengths is customer adaptations of the IMU, such as enabling different sensitivity and accuracy in the IMU’s three different axis (for example, a self-driving car that needs a higher sensitivity and accuracy in the horizontal plane than in the vertical plane), which is expected to give KebNi’s IMUs a cost advantage. Another strength is KebNi’s ability to adapt the IMU and its integration to the unique environment in the application. As a result of product development, KebNi also expects to conduct its IMU operations within three legs.

• Unit sales

• Solution sales

• Own Applications, where we expect information on what the company’s first own application will be within a few months.

Forecasts

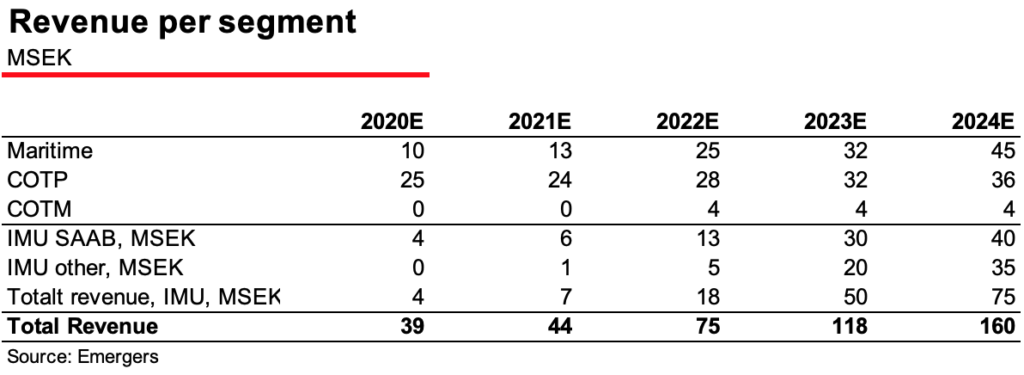

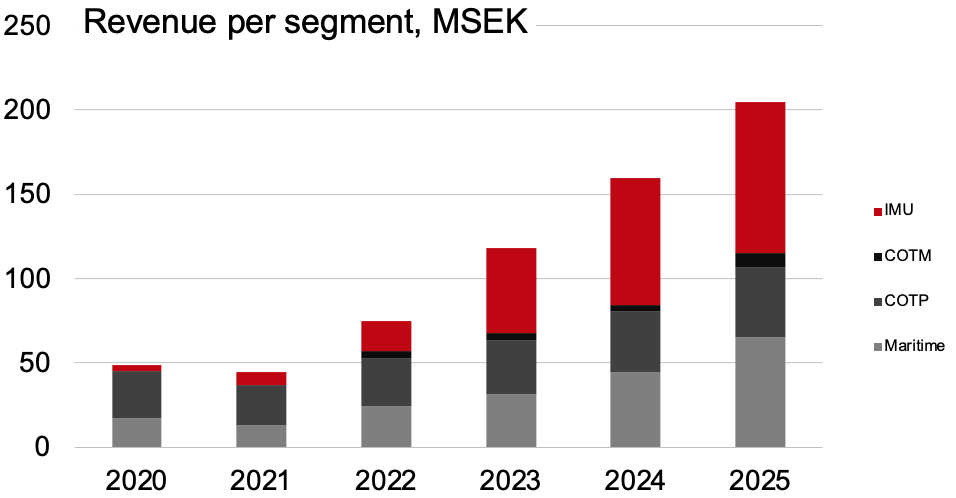

For the SAAB contract, we expect volume deliveries to N-LAW to begin in 2022. We estimate that these could grow to 2,000 units per year in 2024 and that the annual revenues could equal SEK 40 million. According to our estimate, KebNi has in recent years had sales within IMUs of around SEK 1-2 million per year. With the company’s newly developed IMU expected to be completed in Q1 2022, we expect steadily increasing volumes in the coming years, driven by the company’s all three operational legs. In addition, we see good chances for the company to find another high-volume customer, similar to SAAB.

Outlook for the group

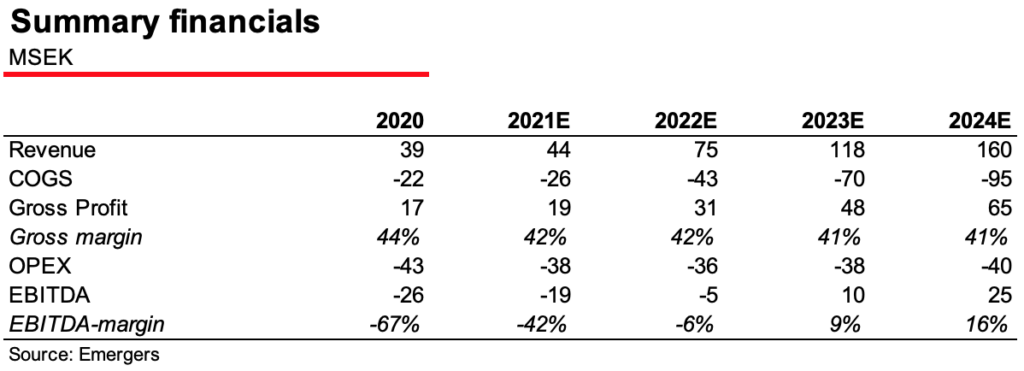

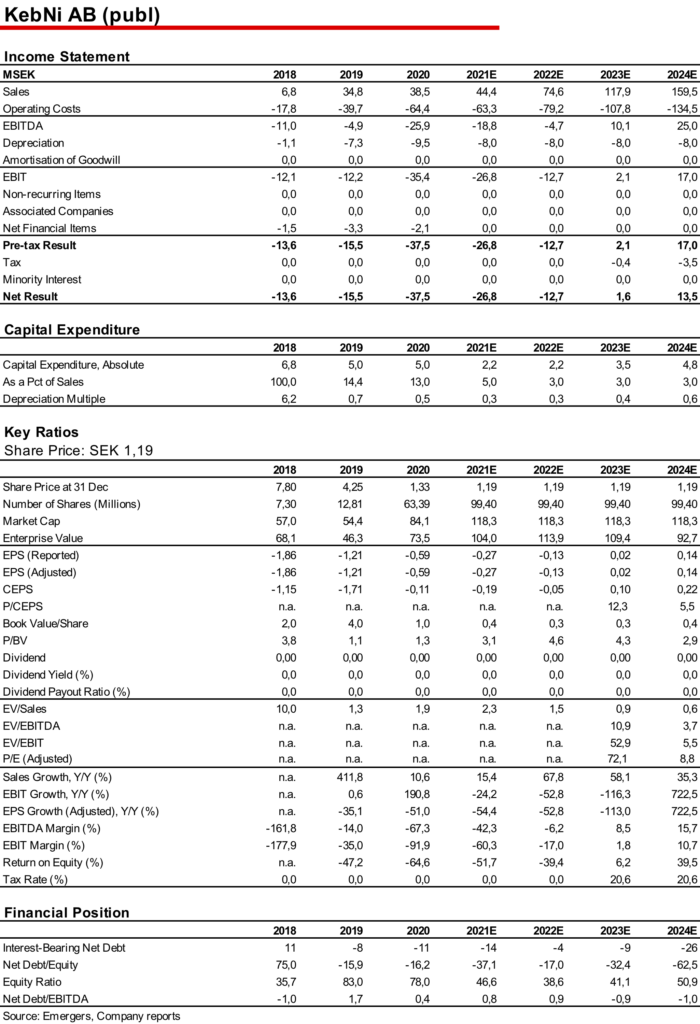

Because Satmission, which today accounts for about two-thirds of KebNi’s sales, was acquired as recently as May 2020, historical figures do not provide much guidance. The company also does not report a gross margin on a quarterly basis and comparability between years is disrupted by capitalized development costs. All in all, this means that any estimate of the company’s costs has a particularly high level of uncertainty.

We estimate a 35% gross margin for directly sold IMUs and a 40-50% gross margin on VSATs. But, since KebNi has a significantly lower gross margin on the IAI business, the SAAB contract will probably squeeze the gross margin when it reaches volume, and KebNi probably will have to work with price when it comes to winning new volume contracts, we believe that it will be difficult for the group to achieve a gross margin in excess of 45% in the next few years. With OPEX of SEK 37 million, a turnover of SEK 90 million will therefore be required to achieve CF breakeven.

Scenario analysis 2025

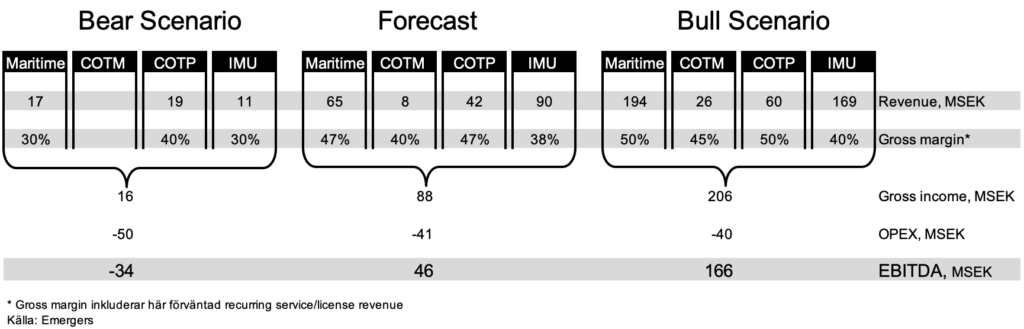

A scenario analysis of the long-term outlook for the company in 2025 shows a continued EBITDA loss of SEK -34 million in our Bear Scenario and EBITDA of SEK 171 million in our Bull Scenario. The calculations are based on the following main assumptions.

Bear Scenario

- In Maritime, KebNi does not succeed in raising volumes above the current level, nor does it succeed in raising prices significantly. This also means that it fails to raise the gross margin.

- KebNi does not continue to invest in COTM Land and does not achieve success with its product, which is too expensive for the commercial market.

- COTP Land grows more slowly than the market and remains around today’s level with a healthy gross margin of 40%.

- The contract with SAAB gets going but achieves one-quarter of the expected volume. Other volume transactions fail to materialize, which means other IMU sales at the current level.

Bull Scenario

- With the company’s well-invested product portfolio within Maritime and increased sales efforts, it achieves a 7.5% market share corresponding to 75 units and succeeds in raising prices.

- KebNi has invested an estimated SEK 15 million in developing COTM Land for public-sector and military customers, which means that the business is in the roll-out phase in 2025 with sales of 25 units and a healthy gross margin of 45%.

- COTP Land succeeds in expanding from the Russian market and gains market shares.

- IMU sales to SAAB exceed the volume in our base scenario, and there is one further high-volume customer.

- The company also succeeds in developing a business with recurring service and licence revenues within all product lines, which in 2025 represent 10% of new sales, with a continuously growing base.

Financing

Following KebNi’s rights issue in Q4 2020 of SEK 45 million, the company was able to repay its loan to Formue Nord and start the year with cash of around SEK 10 million. However, scheduled investments this year, expected operating losses in 2021, and the first partial payment of the earnout for Satmission of an estimated SEK 3 million in Q1 2022, will however take up a significant part of the most recent issue.

After a capital injection of SEK 38 million, our model shows that there is a possibility that the financing will be sufficient until the company achieves a positive cash flow in 2023E. In addition, large orders and customer contracts may open up more ways to finance operations rather than further diluting the shareholders.

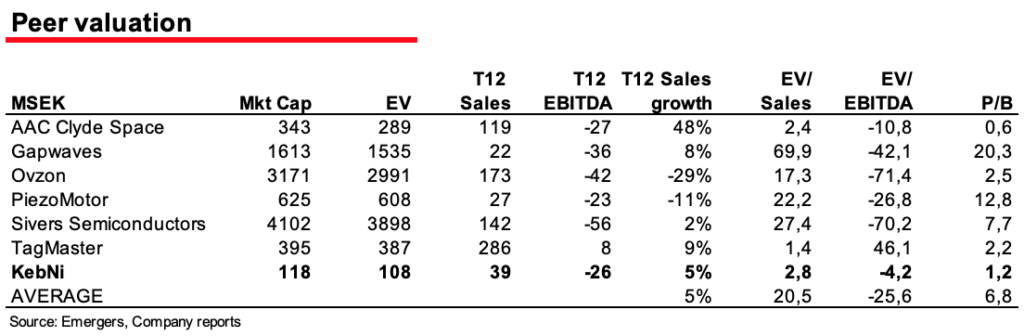

Valuation – plenty of upside potential

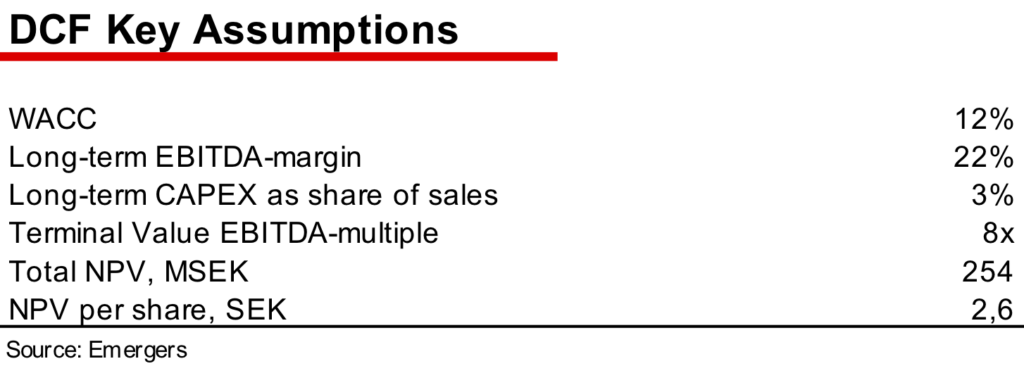

KebNi has a long period of losses behind it, and this is expected to continue for at least two years. At the same time, the company has made, and continues to make, significant investments in technology development that have not yet been translated into commercial contracts. Any valuation of the company is therefore associated with a particularly high degree of uncertainty. This analysis uses a two-pronged approach using both target multiples for future expected sales and profit (EV/sales, EV/EBITDA and P/E) and a present value calculation of future cash flows (DCF) discounted to the present with a discount rate (WACC) of 12%.

Since our forecast shows that the company can achieve these future gains without additional capital contribution, we do not calculate for any further dilution. All in all, our calculations show a fair value of SEK 2.6 (DCF) – 2.8 (multiples) per share on an 18-24 month horizon using our Base Case scenario.

Strategic issues for new management to resolve

KebNi is facing a number of strategic issues that will be crucial for both how the company best allocates its resources and development efforts in the short term, and for the company’s long-term survival.

- How to generate recurring revenue?

- Service and support: The company currently lacks recurring revenues, which means there are major fluctuations between different quarters and years, and no earnings stability. Like many other product-selling companies, KebNi should be able to develop an aftermarket business with service and support. It is not uncommon for manufacturing companies with a well-developed service and support business to create a recurring aftermarket business corresponding to 20% of sales. At present, the company has no such in recurring revenues.

- Software licences: Both VSAT and IMU have important software features. How can the company generate recurring licence revenues based on that software?

- How could KebNi go from box delivery to solutions provider? KebNi’s end customers do not primarily want a stabilized satellite antenna platform but a satellite connection for data transmission. Can or should the company invest in offering a complete solution?

- Follow the development towards flat panel/phased array? Part of the development within VSAT is moving towards a technology called flat panel or phased array. This means that instead of using a classic parabolic dish, the antenna is flat and uses an algorithm to create a beam of radio waves that can be electronically controlled to point in different directions without moving the antenna. KebNi is not currently present in this niche.

- Poor product-market fit for future COTM Land that is probably too expensive for commercial customers. Should KebNi take on the development cost, which is likely to amount to a double-digit number of millions of kronor, to adapt the solution for public-sector customers and military standards?

- Follow developments towards non-geostationary low Earth orbit satellites? This was an initiative started by the previous management, but now seems to have been completely abandoned.

Corporate governance and shareholders

Following the latest issue, KebNi has acquired a clear main owner in the form of Jan Robert Pärsson.

The Chairman of the Board is David Svenn, born in 1983. Svenn has been the chairman and a director since June 19, 2018. David Svenn is a lawyer and former CEO of ASTG AB. He is independent in relation to the company and owns 94,000 shares in KebNi.

Other well-known directors are Jonas Eklind, better known as CEO of Azelio (First North, market capitalization SEK 6,200 million) and Jan Wäreby, former sales manager at Ericsson.

Torbjorn Saxmo took over as CEO on February 9, 2020. Saxmo was previously Head of Marketing & Sales Business Unit Missile Systems at Saab Bofors Dynamics AB in Karlskoga, Sweden.

Things worth bearing in mind

Earnout for Satmission AB

Upon the acquisition of Satmission AB on May 12, 2020, the parties agreed on a price of 2.5 million ASTG Class B shares, valued at approximately SEK 5.5 million. An agreement was also reached on a 3-year earnout model based on Satmission AB’s performance. Payment is based on annual sales, with an accumulated minimum payment of SEK 4.59 million after 3 years. There is no agreed ceiling. ASTG has the right to defer payment until February 2022 for the first years.

Conditional shareholder contribution

In 2015, KebNi received a total of SEK 10 million in conditional shareholder contribution. The contribution is conditional on repayment as soon as the company has unrestricted equity that allows repayment and this is not in conflict with the Swedish Companies Act. The condition of repayment of the contribution has not been set in relation to the company, but only in relation to other shareholders. This means that only the general meeting can decide on repayment of the conditional shareholder contribution, and such repayment must also follow the same rules in the Swedish Companies Act that apply to dividends. Should the general meeting decide on repayment of the conditional contribution, this will be repaid to the contributors. KebNi currently has no plans to repay the shareholder contribution.

Johan Widmark | Tel: 0739196641 | Mail: johan@emergers.se