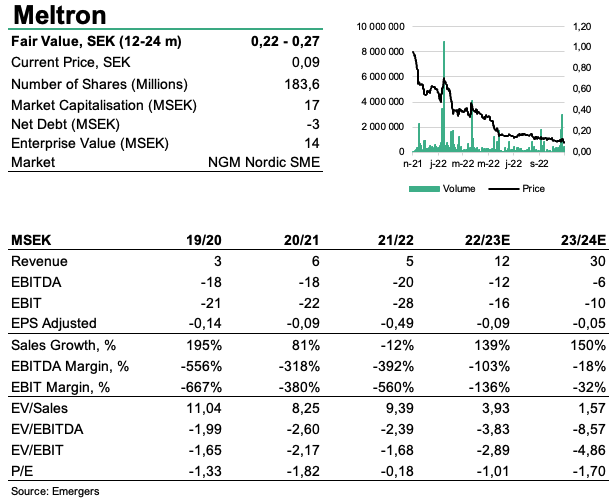

After a cash injection of SEK 11.3m from the completed rights issue, Meltron now has its sights set on positive cash flow through sales growth driven by distributors all over northern Europe. While the high potential in Oman, and a potential cooperation with Huawei remains, we’ve revised our sales estimates for 23/24E and 24/25E and now find support for a fair value of SEK

0.22 – 0.27 per share (0.29 – 0.39) in 12-24 months.

Andreas Eriksson | 2022-11-24 08:00

This commissioned research report is for informational purposes only and is to be considered marketing communication. This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and Emergers is not subject to any prohibition on dealing ahead of the dissemination of investment research. This research does not constitute investment advice and is not a solicitation to buy shares. For more information, please refer to disclaimer.

Cash injection extends runway to positive cash flow

With the aim of raising SEK 16.1m in the recently completed rights issue, which was guaranteed to 64%, subscription rate was somewhat worrying at a mere 22.5% meaning Meltron ended up raising SEK 11.3m while issuing 126 million new shares, diluting non-participating shareholders by 68%. Sales in fiscal year 21/22 amounted to SEK 5m (Jul-Jun), and we estimate that Meltron will need to increase sales to some SEK 40m in order to break even. This means that the company must pick up the pace, if another rights issue is to be avoided. While high-value deals lurk in the distance with global giant Huawei and infrastructure projects in Oman, the short term focus on direct sales and sales through distributors hasn’t yielded much growth so far. Another key focus area for the company has been on lowering costs, which we saw an example of in H1’22 where costs were lowered by 26%. In the upcoming 3–6 months, Meltron will outsource its production which is supposed to lower costs even further, and break even might therefore be reached at lower sales than our estimations.Looking to capitalize on strong macro trends

With a superior lifespan compared to fluorescent lighting, LED is destined to play a major role in the transition towards a more sustainable society. As a consequense of an EU-decision to ban all lighting containing mercury, more than 17 million lighting fixtures will need to be upgraded in Sweden alone. Meltron has continued down the beaten path and signed a new partnership with a Swedish distributor, as a step on the way to building a vast distribution network across northern Europe to get sales going. Being well-positioned in the premium segment of LED-lights, where entry barriers are a bit higher due to the higher cost, Meltron is set to capitalize on the high gross margins if the company can get sales going.

High potential at high risk

While we continue to see considerable potential for Meltron in Oman, where large amounts are now invested in infrastructure projects, the negotiations seem to have been paused, and Meltron’s focus has instead shifted towards northern Europe. With an estimated pick up in sales to SEK 12m during fiscal year 22/23E, we’ve lowered our estimates for 23/24E and 24/25E to SEK 30m (40m) and SEK 50m (60m) respectively, as a result of the longer lead times in Oman. Based on a combined DCF and target multiple approach we see support of a new fair value of SEK 0.22 – 0.27 per share (0.29-0.39) in 12-24 months, while we continue to see plenty of long term opportunities for high-value deals in Oman and with Huawei.

DISCLAIMER