Johan Widmark | 2022-08-05 08:00

Focus to migrate to most high value application area

In the new CEO’s first official communication with shareholders, Julian Read puts emphasis on the ballooning opportunities for microalgae in the biopharma space. Focusing on Antibody Drug Conjugates (ADC), that has risen to rival CAR T as the potential magic bullet in oncology, where 12 ADC drugs have been approved by the FDA so far, we note that several of these approved drugs are based on cyanobacterial toxins, the very potent and close cousin to microalgae.

While pure biopharma license production and a GMP production facility are still some years away, the company now sets out to create revenues from collaborations with pharma companies. This is a first step to expand activities beyond biomass and Omega-3 that are already in scale-up phase. In the long-term however, the high margin nature of the biopharma venture means that it may grow to dominate the company, a development which could be accelerated further by acquisitions.

ADCs quickly catching up to CAR T

Looking closer at the ADC market in the CEO’s crosshairs, we find that ADCs, that comprise of an antibody conjugated to cytotoxic payloads by specially-designed linkers, not long ago was considered to have potential to become the magic bullet in oncology. But they’ve also presented huge challenges to researchers particularly regarding the identification of a suitable combination of antibody, linker, and payload. We also note that ADCs have quickly caught up to CAR T and is now amongst the fastest growing drug classes in oncology.

Today there are 12 ADC drugs approved by the FDA, including Kadcycla for metastatic breast cancer, Polivy for relapsed or refractory diffuse large B-cell lymphoma and Adcetris for treating relapsed or refractory Hodgkin lymphoma. The latest approval was for Tivdak in September 2021 for treating metastatic cervical cancer. With an average price of the mentioned drugs at 101 000 USD per treatment, these are expensive treatments. This can be compared to CAR T, that are more financially and medically intensive treatments, at a cost per treatment around 500 000 USD. In March 2022, market research firm Research & Markets estimated that the global Cancer Antibody Drug Conjugate market will grow to reach 25 BN USD by 2028. Should Simris be able to create a milestone / royalty business in ADC development, based on its closed, horizontal photobioreactor, this would be a significant long-term revenue opportunity for the company.

Far reaching implications for the share

It has long been debated where Simris should allocate its limited resources to best capitalize on all the various and highly dispersed business opportunities that come with owning a world class microalgae production facility. While we expect to see continued biomass deals as the ones press released in the past year, and a pick-up following the re-launch of the Omega-3 this fall, it is now clear that the CEO is gunning for the most ultra-high value opportunity out there, which we also believe to be the one that produces most value for shareholders in the long-term. With the strengthened financials after the combined rights and directed share issues during summer, that raised 25 MSEK before costs, we expect that Simris is fit to pursue affordable bolt-on acquisitions provided they are accretive to the Simris share price.

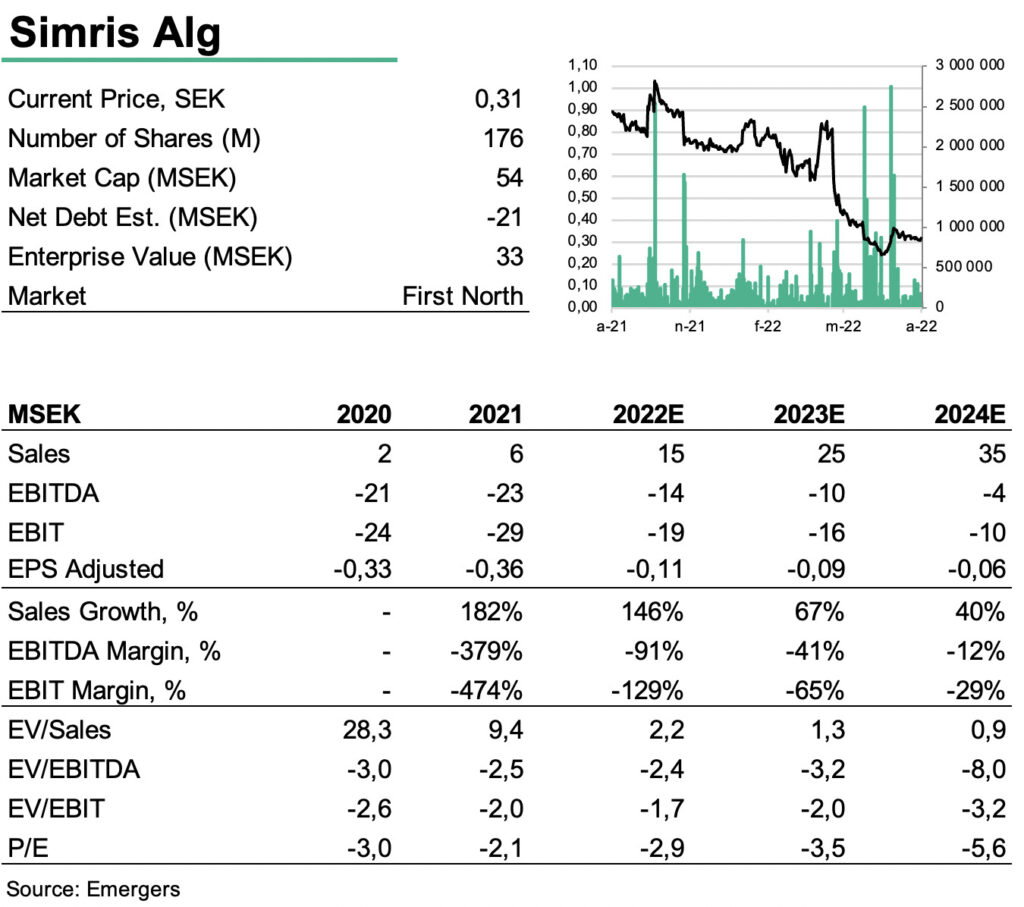

All in all, we continue to see a significant revaluation potential in Simris, and that the triggers are now starting to line up, the most important one would be an accretive M&A deal that can accelerate the venture in the biopharma space. For now, we continue to see an upside risk to our forecast of 25 MSEK in sales in 2023 and 35 MSEK in 2024 with a positive EBITDA by 2025. Supported by only a fraction of listed peer multiples we find support for a fair value of 150 MSEK in 2023 and 210 MSEK in 2024, which translates to 0.85 SEK and 1.19 SEK per share in 2023 and 2024 respectively.

Read more about Simris Alg here

Fourth fucoxanthin order confirms commercial turnaround and sets Simris up for revaluation in 2022

With four orders with a total value of 7.5 MSEK in the last eight months, of which two booked in the first two months of 2022, it is

DISCLAIMER