Johan Widmark | 2022-09-02 08:00 | DISCLOSURE: Emergers parent company Incirrata AB owns shares in Bonzun AB.

Activities with mixed traction in Q2

The revised pricing strategy for Bonzun IVF seems to quickly be generating results, with conversion rates for paying app users up from 43% of users at end of Q1 to 57% at end of Q2. Along with a language expansion to six languages, this has resulted in a 75% increase in paying subscribers, albeit from low absolute levels. As for the iKBT application Bonzun Evolve, KTH Royal Institute of Technology has expanded its collaboration with Bonzun to cover 450 new licenses at the end of Q2. Bonzun Evolve now also comes as a mobile app. With collaborations with the world’s leading fertility network, Fertility Help Hub with 150,000 members in the US and the UK, and approval from the Swedish Social Insurance Agency as organizer of workplace-oriented rehabilitation support, we see a good chance for a pickup in sales growth in H2’22 and 2023.

International Digital Therapeutics (DTx) industry bustling

While Bonzun have taken a severe beating from the current market sentiment, which now rewards near term profits and punish companies with profits far ahead in the future, international players in the DTx industry show a similar or somewhat mixed picture. Just before summer, Moka Care that is building a B2B solution providing the employees of other companies access to mental health therapy, raised USD 15.8 m in a series A led by Left Lane Capital, joined by Singular and Origins. Other DTx company, Pear Therapeutics have seen its share drop c75% in 2022 and has trimmed staff, but is still valued at USD 240m. Other DTx company Akili listed via a SPAC in August 2022, that netted the company USD 163m, which it plans to use to commercialize its video game-based treatment for pediatric ADHD.

Another capital raise on the horison

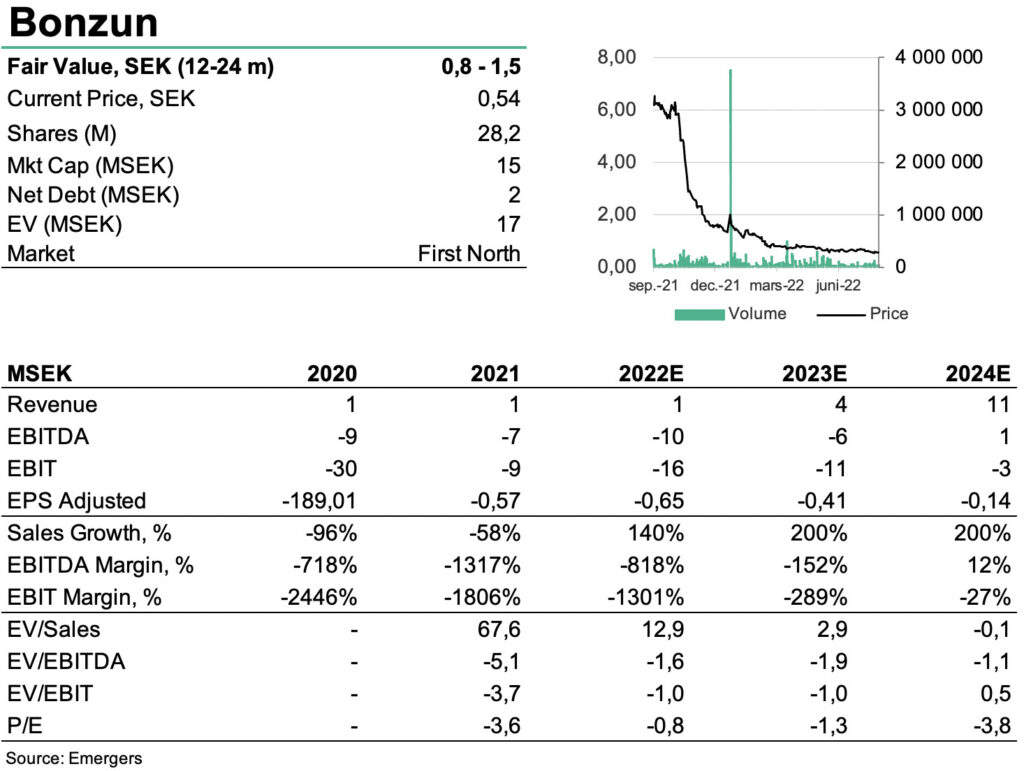

The SEK 2m in debt raised on the day of the report gives Bonzun runway for about one quarter, which means that we’re likely to see some sort of capital raise in the near future. With the share price down c60% year to date, Bonzun provides an interesting entry point for new money looking for exposure to the two megatrends of digital stress management and IVF, in the form of digital IVF support. With some severe cost cutting measures we see a fair chance for Bonzun to turn to positive cash flow in 2024. While we don’t expect the company to raise all the SEK 12-15m needed to reach positive cash flow, half of that would probably be enough to take the company to the next step and stronger momentum that should provide better and more favourable conditions for the next financing round in 2023. Adjusted for a raise in H2’22 we now find a support for a fair value of SEK 0.8-1.5 (1.5-2.5) per share in 12-24 months.

DISCLAIMER

General disclaimer and copyright

This material is not intended to be financial advice. This material has been commissioned by the Company in question and prepared and issued by Emergers, in consideration of a fee payable by the Company. Emergers standard fees are SEK 240 000 pa for the production and broad dissemination of a detailed note following by regular update notes. Fees are paid upfront in cash without recourse. Emergers may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained herein represent those of the research analyst at Emergers at the time of publication. The company has been given the opportunity to influence factual statements before publication, but forecasts, conclusions and valuation reasoning are Emergers’ own. Forward-looking information or statements contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Emergers shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this material. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Emergers’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in this material may not be eligible for sale in all jurisdictions or to certain categories of investors. Investors are encouraged to seek additional information as well as consult a financial advisor prior to any investment decision. Investment in securities mentioned: Emergers has a restrictive policy relating to personal dealing and conflicts of interest. Emergers does not conduct any investment business. Emergers parent company Incirrata AB does hold a position in the security mentioned in this report. The respective directors, officers, employees and contractors of Emergers may have a position in any or related securities mentioned in this report, subject to Emergers’ policies on personal dealing and conflicts of interest. Copyright: Copyright 2021 Incirrata AB (Emergers)

United Kingdom

This document is prepared and provided by Emergers for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the ”FPO”) (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States

Emergers relies upon the ”publishers’ exclusion” from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Emergers does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person.