GRÄNGESBERG EXPLORATION The ongoing preparations for the DFS of Dannemora has now yielded its second upwards revision, a 16% increase in mineral reserves to 30.8 Mt with 32.2% Iron, and over a year’s extension of the life of mine. The >4Mt reserves increase is based on recovering the 21% iron which is in the tailings deposited underground during the last production period, 2012-2015.

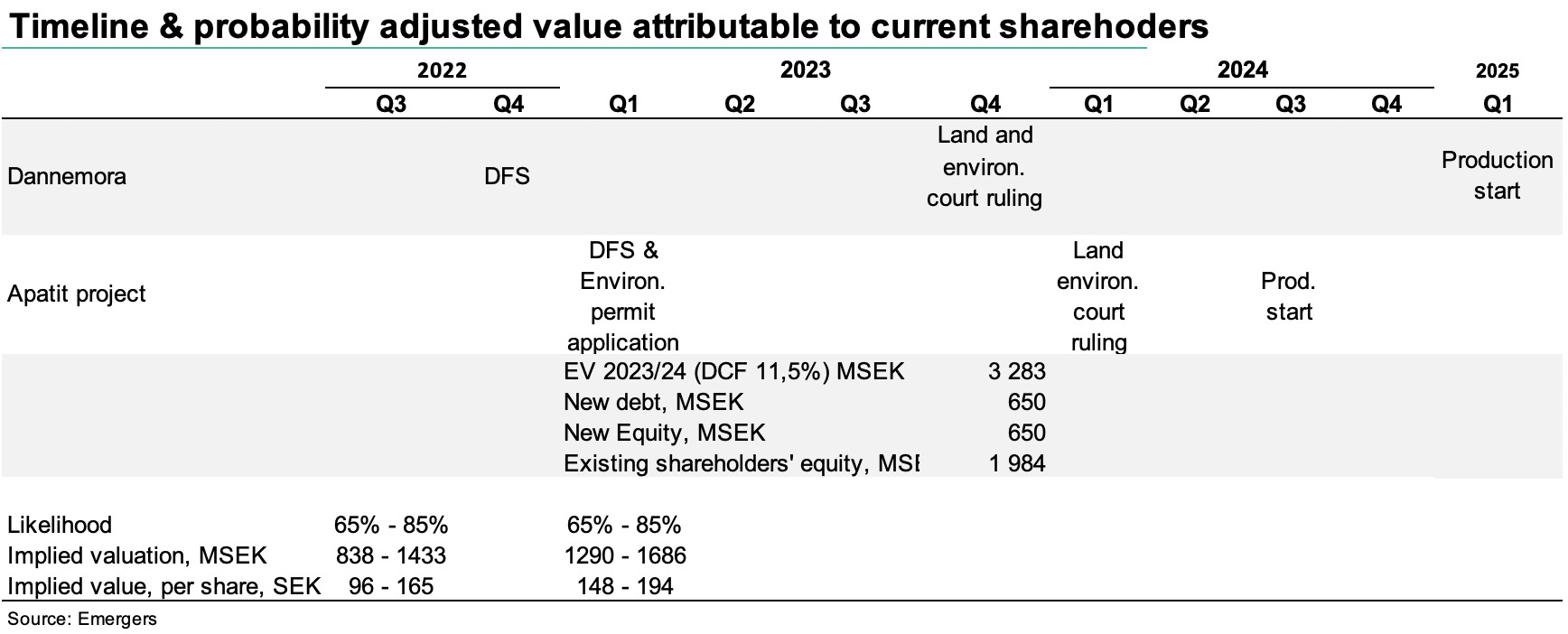

After a revision of our estimates for production profile, FX, life of mine and an increase in power expenses we find only a slight net effect on our fair value, now at SEK 96-165 (98-168) per share in 12-24 months. This leaves room for a considerable revaluation where we see accelerating structural demand for green CO2-free steel, a prolonged supply crisis following Russia’s cut off from Europe and progress with GRANGEX’s DFSs and environmental permits for the two projects as the main catalysts.

Johan Widmark | 2022-09-21 08:00

4Mt of tailings with 21% iron

As the company alluded to already in the PFS in January, it has now found a way to include the tailings deposited underground from the latest production period, into the mineral reserves. While the current plan is to process the tailings continuously over the production period, the company could potentially start with the tailings, as they don’t require crushing and can be put straight into the dressing plant, thereby getting a jumpstart on production. The tailing contains 21% iron, well above planned capacity cutoff at 15%, which also means that OPEX for these >4Mt will be lower than for the ore in the ground.

With regards to costs, the surge in the Nordic power price is being felt in the cost projections for Dannemora, which is to be fully electrified, where we now expect a 3-4 USD/t cost increase attributable to a higher long term power price. The 16% hike in mineral reserves also comes with a 1.2 percentage point reduction in concentration, to from 33.4% to 32.2%, which gives Dannemora a slightly lower-for-longer production profile. Most importantly we note a continued weakening of the SEK, up 20% year to date, benefitting the revenue side in our model.

Surge in phosphate rock price continues

Simultaneously, we note that the DFS and the environmental permit application for the Apatite project, which we earlier expected to be presented and filed in Q3’22, now will likely be delayed 1-2 quarters as resources are focused on Dannemora. As for prices, we’ve seen a continued pullback in the iron ore prices while the prolonged war in Ukraine and subsequent trade restrictions have continued to push prices of phosphate rock further, where prices have surged to over 300 USD/t, of which we include only a small portion into our valuation model for the Apatite project.

Along with a structural long-term growth in demand for green CO2 free iron ore and a prolonged supply crisis following Russia’s cut off from Europe we find both a strong fundamental case as well as a bright backdrop for the projects. With the major financing round for these projects most likely during H1’23, we now expect production start for the Apatite project sometime early/mid 2024 and production start in Dannemora around winter ‘24/25.

All in all, we now find support for a NPV at SEK 3.3bn and a repayment within three years. Reduced by project financing for both the Apatite project and Dannemora, where we expect debt of SEK 650m and new equity of SEK 650m, approximately SEK 2bn remains attributable to today’s shareholders. Risk adjusted with an estimated probability of successfully passing the next two years’ milestones of 65-85% per year, this provides support for a fair value today of around SEK 840-1,430m or SEK 96-165 (98-168) per share.

DISCLAIMER